Discover 3 KRX Growth Companies With High Insider Ownership And At Least 22% Return On Equity

The South Korean stock market has shown resilience, advancing in consecutive trading days and positioning the KOSPI just below the 2,730-point mark. This positive momentum reflects a generally upbeat global outlook and favorable domestic financial performances. In this context, companies with high insider ownership can be particularly compelling as they often demonstrate aligned interests between management and shareholders, potentially enhancing stability and confidence in turbulent times.

Top 10 Growth Companies With High Insider Ownership In South Korea

Name | Insider Ownership | Earnings Growth |

ALTEOGEN (KOSDAQ:A196170) | 26.6% | 73.1% |

Global Tax Free (KOSDAQ:A204620) | 18.1% | 72.4% |

S&S Tech (KOSDAQ:A101490) | 21.6% | 44.1% |

Fine M-TecLTD (KOSDAQ:A441270) | 17.3% | 36.4% |

Park Systems (KOSDAQ:A140860) | 33.1% | 35.8% |

Seojin SystemLtd (KOSDAQ:A178320) | 26.4% | 48.1% |

UTI (KOSDAQ:A179900) | 34.1% | 122.7% |

HANA Micron (KOSDAQ:A067310) | 19.8% | 76.8% |

INTEKPLUS (KOSDAQ:A064290) | 16.3% | 77.4% |

Techwing (KOSDAQ:A089030) | 18.7% | 118.2% |

Let's review some notable picks from our screened stocks.

ALTEOGEN

Simply Wall St Growth Rating: ★★★★★★

Overview: ALTEOGEN Inc. is a biopharmaceutical company engaged in developing long-acting biobetters, proprietary antibody-drug conjugates, and antibody biosimilars, with a market capitalization of approximately ₩15.06 billion.

Operations: The company generates revenue through the development of long-acting biobetters, proprietary antibody-drug conjugates, and biosimilar antibodies.

Insider Ownership: 26.6%

Return On Equity Forecast: 45% (2027 estimate)

ALTEOGEN, a South Korean biotech firm, has recently become profitable and is poised for significant growth with earnings expected to increase by 73.06% annually. Despite a highly volatile share price in the past three months, its revenue growth rate at 48.3% per year outpaces the national market's 10.3%. However, shareholder dilution occurred over the last year, and it trades at 68.9% below estimated fair value. The company presented at the Macquarie Asia Conference in May and will report Q1 results on May 29, 2024.

Take a closer look at ALTEOGEN's potential here in our earnings growth report.

The valuation report we've compiled suggests that ALTEOGEN's current price could be inflated.

CLASSYS

Simply Wall St Growth Rating: ★★★★★☆

Overview: CLASSYS Inc. operates globally in the provision of medical aesthetics devices, with a market capitalization of approximately ₩3.08 billion.

Operations: The firm generates revenue from the global sale of medical aesthetics devices.

Insider Ownership: 10.1%

Return On Equity Forecast: 28% (2027 estimate)

CLASSYS Inc., a South Korean company, is demonstrating robust growth with its revenue forecast to increase by 21.3% annually, outpacing the national market's 10.3%. Earnings have expanded by 25.9% annually over the past five years and are expected to continue growing at 22.18% per year. Despite its earnings growth trailing the broader Korean market's projected 29%, CLASSYS maintains a strong insider ownership structure without significant selling in recent months, indicating confidence from those closest to the company. However, it faces challenges with highly volatile share prices and shareholder concerns over governance highlighted in recent annual meetings.

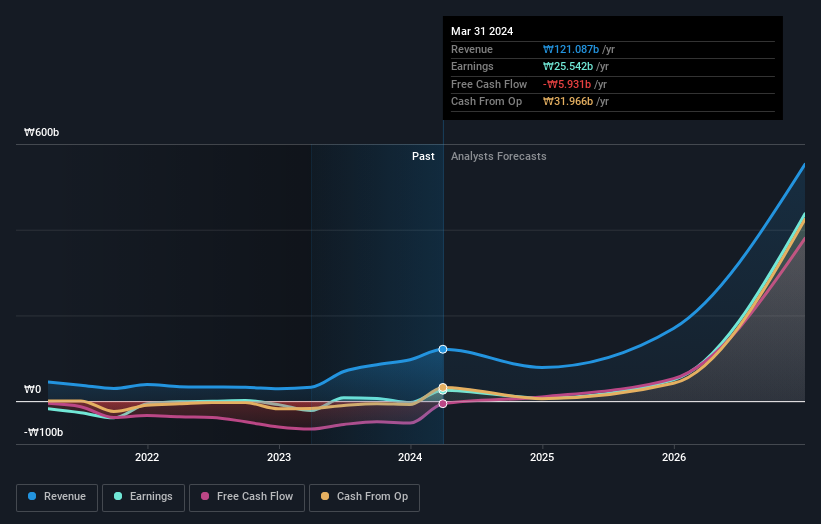

Doosan

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Doosan Corporation operates in sectors including heavy industry, machinery manufacturing, and apartment construction across regions such as South Korea, the United States, Asia, the Middle East, and Europe with a market capitalization of approximately ₩3.08 billion.

Operations: The company's revenue is derived from sectors such as heavy industry, machinery manufacturing, and apartment construction across various global regions including South Korea, the United States, Asia excluding South Korea, the Middle East, and Europe.

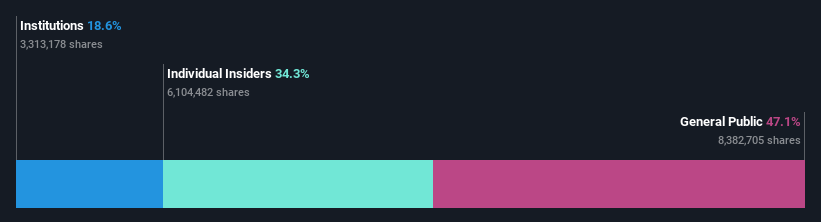

Insider Ownership: 34.3%

Return On Equity Forecast: 22% (2027 estimate)

Doosan Corporation, despite a highly volatile share price, is on a path to profitability with expectations to turn profitable within three years. Recent earnings show significant improvement, with first-quarter sales rising to KRW 180.97 billion from KRW 169.05 billion year-over-year and net income reaching KRW 4.98 billion after a previous loss of KRW 38.68 billion. However, its revenue growth at 3.6% per year lags behind the broader Korean market forecast of 10.3%. The company's return on equity is anticipated to be strong at 22.2% in three years, reflecting potential for substantial efficiency gains in capital usage.

Summing It All Up

Click here to access our complete index of 82 Fast Growing KRX Companies With High Insider Ownership.

Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Searching for a Fresh Perspective?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include KOSDAQ:A196170KOSDAQ:A214150KOSE:A000150 and

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com