Yahoo Finance

Yahoo Finance Why You Should Retain CF Industries (CF) in Your Portfolio

CF Industries Holdings, Inc. CF is expected to benefit from healthy nitrogen fertilizer demand in major markets and lower natural gas costs amid headwinds from lower nitrogen prices.

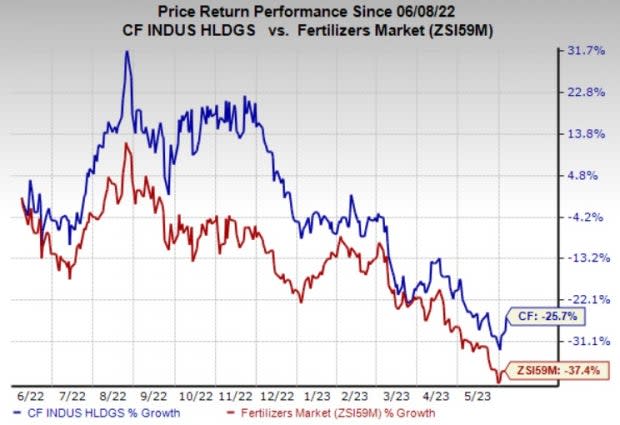

The company’s shares are down 25.7% over a year compared with the 37.4% decline of its industry.

Image Source: Zacks Investment Research

Let’s find out why this Zacks Rank #3 (Hold) stock is worth retaining at the moment.

Higher Nitrogen Demand Bodes Well

CF Industries is well-placed to gain from rising global demand for nitrogen fertilizers, driven by significant agricultural demand. Higher crop commodity prices are contributing to healthy demand globally. Industrial demand has also recovered from the pandemic-related disruptions. High levels of corn planted acres in the United States and favorable farm economics are likely to drive the demand for nitrogen in North America. Increased planted corn acres, higher crop prices and healthy farm economics are expected to drive urea demand in Brazil. The company also expects India to be one of the world’s biggest urea importers this year with frequent urea tenders in the second half.

The company is also expected to benefit from lower natural gas prices. CF Industries witnessed higher year-over-year costs in 2022, leading to a rise in its cost of sales. Natural gas costs also increased to $6.62 per MMBtu in the first quarter of 2023 from $6.48 per MMBtu in the year-ago quarter. However, the company expects a significant decline in natural gas costs in the second quarter. Lower natural gas costs are expected to lead to a decline in the company's cost of sales.

CF Industries also remains committed to boosting shareholders’ value by leveraging strong cash flows. It generated operating cash flows of roughly $3.9 billion and a free cash flow of around $2.8 billion in 2022. The company also returned $1.65 billion to shareholders through share repurchases and dividends in 2022. It also bought back more than 1 million shares for $75 million in the first quarter of 2023. The company’s board has authorized a new $3 billion share repurchase program, which will commence upon completion of the existing share repurchase program and run through the end of 2025.

Lower Nitrogen Prices a Concern

CF Industries faces headwinds from lower nitrogen prices. Global nitrogen prices have declined since the beginning of 2023. Higher global supply availability driven by higher global operating rates due to lower global energy costs has resulted in a decline in prices. Lower average selling prices weighed on CF's top line in the first quarter. The weak pricing environment is expected to continue in the second quarter. Lower pricing is expected to hurt the company’s sales and margins.

CF Industries Holdings, Inc. Price and Consensus

CF Industries Holdings, Inc. price-consensus-chart | CF Industries Holdings, Inc. Quote

Stocks to Consider

Better-ranked stocks worth considering in the basic materials space include L.B. Foster Company FSTR, Gold Fields Limited GFI, and Linde plc LIN.

L.B. Foster currently carries a Zacks Rank #1 (Strong Buy). The Zacks Consensus Estimate for FSTR's current-year earnings has been stable over the past 60 days. You can see the complete list of today’s Zacks #1 Rank stocks here.

L.B. Foster’s earnings beat the Zacks Consensus Estimate in each of the last four quarters. It has a trailing four-quarter earnings surprise of roughly 140.5%, on average. FSTR has gained around 5% in a year.

Gold Fields currently carries a Zacks Rank #2 (Buy). The Zacks Consensus Estimate for GFI’s current-year earnings has been revised 23.5% upward in the past 60 days.

The consensus estimate for current-year earnings for GFI is currently pegged at $1.05, reflecting an expected year-over-year growth of 8.3%. Gold Fields’ shares have popped roughly 63% in the past year.

Linde currently carries a Zacks Rank #2. The Zacks Consensus Estimate for LIN’s current-year earnings has been revised 4.4% upward in the past 60 days.

Linde beat Zacks Consensus Estimate in each of the last four quarters. It delivered a trailing four-quarter earnings surprise of 6.9% on average. LIN’s shares have gained roughly 10% in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CF Industries Holdings, Inc. (CF) : Free Stock Analysis Report

Gold Fields Limited (GFI) : Free Stock Analysis Report

L.B. Foster Company (FSTR) : Free Stock Analysis Report

Linde PLC (LIN) : Free Stock Analysis Report