Why China will keep its important role in global supply chains: MSCI

MSCI remains upbeat on China opportunities.

Long and finely tuned supply chains have been integral to modern business strategies for decades. But as geopolitics, macroeconomics and lessons from the Covid-19 pandemic change the landscape, many companies are rethinking their manufacturing approaches to adopt nearshoring, friendshoring, reshoring or China-plus strategies.

For more than four decades, just-in-time manufacturing and lean-inventory systems fuelled a relentless drive toward cost cutting and rapid production, helping multi-national firms lift margins in a fiercely competitive and increasingly global marketplace.

But global priorities are changing as companies de-emphasise thrift and speed in search of resilience. Today’s supply chains must be more diverse and transparent to help mitigate risk, while offering enough agility to cope with fluid circumstances.

Will China’s manufacturers lose out as companies reassess how they source and assemble goods? Are there implications for investors’ asset allocations?

MSCI research analysts Wei Xu and Manish Shakdwipee looked into these questions in depth and found that the answers are not as straightforward as they may appear. In fact, several industries are likely to remain heavily dependent on China for the foreseeable future.

Resilience through R&D

China’s historical supply-chain advantage was low labour costs, but modern manufacturing ecosystems depend on far more than cheap wages. Skill levels, automation, advanced materials and logistics networks all play a growing role, and China has kept pace on all measures1.

Policy-driven investment and commercial spending on research and development (R&D) have supported advances in education and technological innovation. After rapid y-o-y expansion over the past three decades, China’s total R&D spending has hit US$660 billion in 2021.2

These investments have been concentrated in tech- and resource-driven manufacturing, cementing China as a mainstay of manufacturing in numerous industries. The country dominates supply chains in sectors such as computers, communications and electronic equipment, machinery, automotive tech, medicines, raw-chemical materials and metal products. In the short term, companies in these sectors could face considerable challenges with relocating supply chains out of China.

China has also developed key infrastructure to support the manufacturing ecosystem, including telecommunications, data centers, industrial parks and logistics networks. These facilitate the kind of high-efficiency and cost-effective production that is critical to modern, resilient supply chains.

Through 2021, China installed more industrial robots than the whole rest of the world.

According to MSCI analysis, the US remains the leader in global technology by index weight and revenue exposure. However, China’s revenue exposure to transformative technologies exceeds the rest of the emerging market (EM) universe combined.

China’s footprint in high-end manufacturing and innovative technologies could make the country more critical, not less, for companies in these sectors.

Natural resources bolstering China’s position

China’s dominance of certain natural resources also adds to its resilience in global supply chains. At extraction or processing stages, Chinese firms are integral to the supply of critical materials for industries such as clean energy and technology, advanced electronics and healthcare. Compared to other export-dependent industries, companies in these sectors inevitably have less flexibility for moving supply chains out of China in the short to medium term.

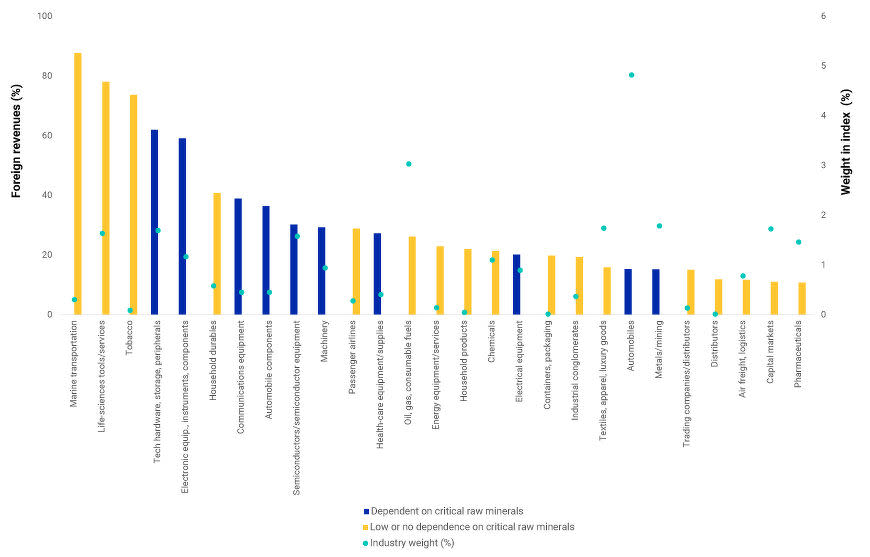

After examining industries in China that derive more than 10% of their revenue from other countries, and matching those with ones that depend on critical minerals, 10 stand out as likely to struggle with moving production lines out of China. These include industries such as technology hardware, electronic and communications equipment, automobile components and machinery.

Ten industries in the MSCI China Index had higher dependence on China’s critical raw minerals

Data as of Sept 29, 2023

MSCI’s analysis highlights two key points for global investors:

China is, and will likely remain, very important in global supply chains.

Certain industries and investment themes that are highly dependent on China’s resources and production capacities could be more exposed to geopolitical risk or sentiment as well as the costs and challenges of trying to mitigate those risks by moving supply chains into other countries.

The reconfiguration of global supply chains is a complex topic, and the impact on specific industries and markets will vary significantly. Looking past headlines to understand the data around China's evolving role in global supply chains can help global investors make more informed decisions.

To find out more about investing in emerging markets, please visit the webpage.

[1] Rosemary Coates, Michael Gherman and Rafael Ferraz, “Global Labor Rate Comparisons,” Reshoring Institute, accessed on Dec 5, 2023.

[2] OECD, “Gross domestic spending on R&D (indicator), accessed on Dec 18, 2023.

See Also:

Click here to stay updated with the Latest Business & Investment News in Singapore

Get in-depth insights from our expert contributors, and dive into financial and economic trends