Yahoo Finance

Yahoo Finance What's Going On With Apple?

In a market-moving announcement this morning, it was revealed that Apple AAPL, one of the most widely-held stocks, has witnessed demand at a level less than initially expected.

Needless to say, it’s a massive development.

The increased demand expected for the newest iPhone on the block, the iPhone 14, has yet to show.

Now, with demand caving in, the tech titan has slashed its original plans to ramp up the production of its legendary product.

Of course, investors were spooked; Apple shares experienced adverse price action in pre-market trading, spoiling the fun.

With Apple being the largest holding in the S&P 500, the negative reaction has played spoilsport in a primarily green market today.

Let’s take a closer look into how the legendary technology titan currently stacks up.

Share Performance & Valuation

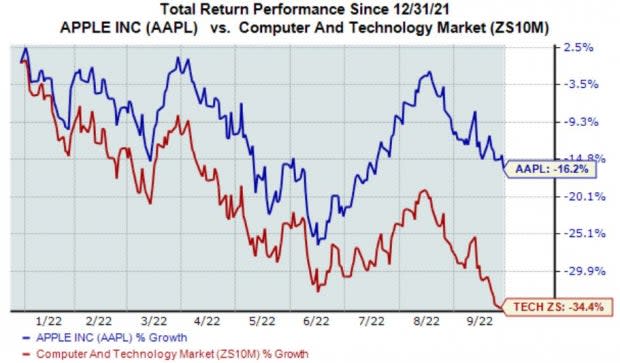

Year-to-date, it’s been a rough ride for AAPL shares, down roughly 16%. Still, the performance widely outperforms its Zacks Computer & Technology Sector, which is down more than 30%.

Image Source: Zacks Investment Research

However, Apple has been a stellar investment even after the rocky 2022, up a triple-digit 170% over the last three years and crushing its Zacks Sector’s performance.

Image Source: Zacks Investment Research

Still, Apple shares may not entice value-focused investors, bolstered by its Style Score of a D for Value.

Further, the company’s 24.9X forward earnings multiple is well above the five-year median of 22.9X and reflects a somewhat rich 20% premium relative to its Zacks Sector.

Image Source: Zacks Investment Research

King of Cash Flow

Apple is the undisputed heavyweight champion of free cash flow – AAPL reported the highest quarterly free cash flow of any S&P 500 company in Q2.

The tech titan’s free cash flow was reported at a stellar $20.8 billion, good enough for a solid 9.4% uptick from year-ago quarterly free cash flow of $19 billion.

Apple has a very favorable free cash flow trend, as seen in the chart below.

Image Source: Zacks Investment Research

The company’s free cash flow speaks volumes about its financial health, telling us it can easily wipe out debt and fuel growth.

Quarterly Performance

Apple has a mighty-strong earnings track record; the company has exceeded the Zacks Consensus EPS Estimate in 19 of its previous 20 quarters. Just in its latest print, the mega-cap giant posted a 5.3% bottom-line beat.

Top-line results paint precisely the same positive story; AAPL has exceeded the Zacks Consensus Sales estimate in 19 of its last 20 quarters.

Below is a chart illustrating the company’s revenue on a quarterly basis.

Image Source: Zacks Investment Research

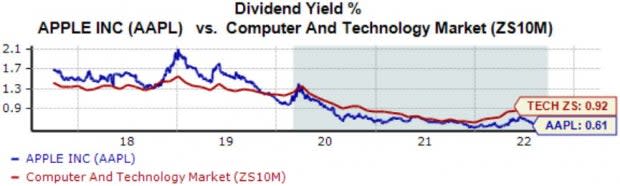

Small Income Stream

Dividends are a significant perk that all investors love. After all, there are few things sweeter than receiving income from your investments.

Apple’s 0.6% annual dividend yield is undoubtedly underwhelming, below its Zacks Computer and Technology Sector average of 0.9%.

Image Source: Zacks Investment Research

Still, while the yield may be low, the company carries a strong 7.7% five-year annualized dividend growth rate.

Bottom Line

While the recent news of expected demand faltering is disheartening, the company is still positioned nicely with its free cash flow strength and its strong earnings track record.

Further, Apple shares have displayed inspiring relative strength year-to-date, even after today’s hiccup.

Still, the company’s valuation levels don’t appeal to value-focused investors, typical of many technology stocks.

Apple AAPL is a Zacks Rank #3 (Hold) paired with an overall VGM Score of a B.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Apple Inc. (AAPL) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research