Yahoo Finance

Yahoo Finance United Engineers Limited - Will Charoen privatise United Engineers?

8/9/2014 – Oversea-Chinese Banking Corporation (OCBC) has announced that it is in talks with Thailand billionaire Charoen Sirivadhanabhakdi and his wife to sell its entire 36% stake in United Engineers.

Bloomberg reported this news on August 21 which led United Engineers' stock price to jump 12%.

It is now trading at around S$2.80, a 58% surge in price this year.

Investor Central had reported the possibility of stake sale by OCBC in February 2013 when United Engineers took control of WBL Corporation.

Our headline questions was "Is it next in OCBC's sale of non-core assets?"

As it turned out, OCBC sold its stake in Fraser & Neave first.

Meanwhile, United Engineers has announced the divestment of its automotive business, a division of WBL Corp, to StarChase Motorsports (Singapore) Pte Ltd for S$455 mln.

It will book a gain of S$17.1 mln

The company had highlighted in January that it would sell non-core assets acquired from WBL Corp.

On August 5, 2014, UEM announced the divestment of assets and liabilities of MFS Technology for S$124 mln, where it has a 57% effective interest through its 67.6%-owned WBL.

The company has granted the purchaser, PE funds Novo Tellus and Navis, an exclusivity period up to September 5 or the execution of the Sale and Purchase Agreement, whichever came first.

Commenting on the outlook during its Q2 announcement, the Group said that property sector cooling measures implemented by the Singapore and Chinese governments would continue to affect its sales and as such, it will remain cautious in bidding for new land sites.

However, it remains optimistic about the engineering and construction businesses as demand in Singapore for 2014 is expected to remain relatively strong.

But high labour cost is still a hurdle when it comes to costs saving.

It will try to raise productivity through improving its work processes and introducing new technology in its operations and project execution.

CIMB Research has maintained its HOLD rating but raised the target price from S$2.22 to S$2.53 due to potential upside from a takeover offer.

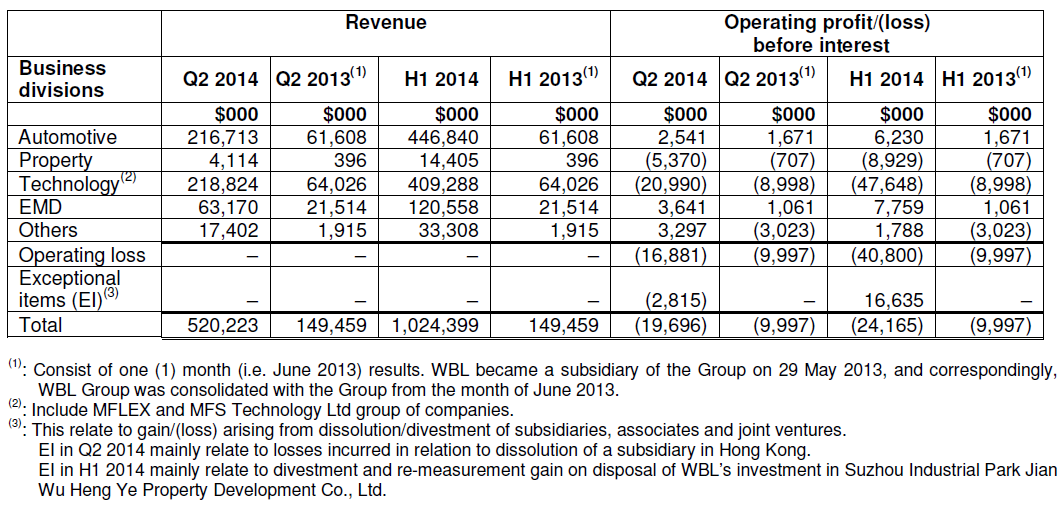

The company just announced earnings for Q2 FY14:

Revenue: +302% to S$1.2 bln

Profit: +165% to S$40.8 mln

Cash flow from operations: S$108.1 mln vs S$19.9 mln

Revenue grew mainly due to full revenue recognition for Austville Residences which is based on the completion-of-construction accounting method.

The progressive revenue recognition from the property sales at Eight Riversuites also contributed to the higher revenue.

Revenue was also higher due to a 252% jump in the automotive segment to S$216.7 mln.

Have a look at the table below for segment revenues and operating profits.

Investor Central. Asian insights for global investors. We ask the tough questions of Asian companies which global investors need answers to.

1. Will Charoen privatise the company?

Thailand billionaire Charoen Sirivadhanabhakdi will probably buy OCBC's 36% stake in the Group.

This would trigger a mandatory takeover offer for United Engineers under Singapore rules.

But in order to take United Engineers private, it will have to acquire a 90% stake.

Does Charoen has any such intentions?

2. What price should Charoen pay for the stake?

CIMB Research says that Charoen is a savvy investor who will not overpay for assets.

Based on the past M&A transactions in the property space at average 0.8 times Price-to-RNAV, it estimates that Charoen could pay 0.8 times to 0.9 times RNAV.

However, it is currently trading 1.06 times its book value based on book value per share of S$2.69 (Source:Reuters) and market price of S$2.84.

Total number of questions in the full story: 8)

We have invited the company to an on-camera interview, and/or to reply to our questions in writing.

We have had communication with the company's PR firm, however at publication time we had not received a reply.

We will update this report if we do.

Legal notice

While our purpose is to ask the questions which the man on the street would ask, and to help the everyday investor make informed investments, please note that:

Our reports and presentations ('our contents') are not investment advice nor should they be construed as investment advice or any recommendation of any kind; nor meant to cast allegations or insinuations of any kind against any individuals or entities. Before acting on the material in our contents, you should either seek independent advice tailored to your particular circumstances and intentions or rely on your own judgement.

Our reports and presentations express our observations, opinions and theoretical analysis based on the facts that we have gathered or have been provided to us. While we endeavour to ensure that our contents are accurate and are presented in good faith, we cannot and do not warrant the accuracy, adequacy or completeness of the material or that the material is suitable for its intended use; and we disclaim any such warranties express or implied that may be presumed by any party; neither do we take responsibility for the views of companies or other stakeholders or observers or sources quoted or hyperlinked in our contents. While every precaution has been taken in the preparation of our contents, we (and our principals) shall not be liable for any losses or damage or inconveniences due allegedly to errors or omissions in any facts or due allegedly to reliance on our contents in any way whatsoever; nor for any damage to any computer hardware, date information or materials allegedly caused by our contents.

All expressions of opinion and observations in our contents are subject to change without notice and we do not undertake a duty to update and supplement our contents or the information contained herein in the event we obtain any further or more complete information.

©2014 Investor Central® - a service of Hong Bao Media