Yahoo Finance

Yahoo Finance

SI Research: Hi-P International – Is The High Payout Sustainable?

Singapore’s manufacturing sector remains a major growth driver for the economy. According to data from the Economic Development Board, overall output rose 11.1 percent in May 2018, defying expectations of a slowdown.

While the growth was not across the board, the key electronics cluster registered a 17.1 percent expansion in output. Semiconductors performed well with a robust growth of 26.9 percent, up from 15 percent in April 2018. The rest of the electronic segments registered a decrease in output.

Since our previous coverage in July 2017, Hi-P International’s (Hi-P) share price has increased by over 40 percent to $1.30 at the time of writing. Although the current price is a steep drop from its 52-week high of $2.72 recorded in March 2018, investors who picked up their shares at below a dollar each in July last year should be more than satisfied as Hi-P also announced dividends of $0.19, $0.02 and $0.04 in August 2017, November 2017 and May 2018 respectively.

Currently, Hi-P ranks the highest in terms of dividend yield at 19.8 percent, far ahead of runner up, Asian Pay Television Trust at 15.6 percent. Meanwhile, the REIT with the highest dividend yield is Lippo Malls Indonesia Retail Trust at 10.2 percent.

The Business

Hi-P started out as a tooling specialist in Singapore almost 40 years ago and has since grown to become one of the region’s largest and fastest-growing integrated contract manufacturers.

With a total of 13 manufacturing plants strategically located across China, Poland, Singapore and Thailand, Hi-P is able to provide a one-stop solution to customers in various industries. The group’s services are engaged by many of the world leaders in mobile phones, tablets, household and personal care appliances, computing and peripherals, lifestyle, medical devices and industrial devices.

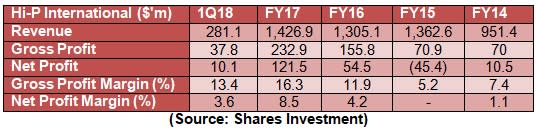

Improving Financial Performance

Over the past four years, Hi-P’s revenue had increased by around 50 percent while FY17 net profit was more than 11 times that of FY14. In 1Q18, Hi-P reported revenue of $281.1 million, a 15.1 percent increase from 1Q17. The higher revenue led to a 20 percent increase in 1Q18 net profit to $10.1 million.

Going forward, the outlook is not too bright as the International Data Corporation’s (IDC) Worldwide Quarterly Mobile Phone Tracker, showed that worldwide smartphone shipments declined by 0.5 percent in 2017, marking the first year-over-year decline for the market. Meanwhile, shipment volumes could return to low single-digit growth in 2018 and the overall market is expected to experience a compounded annual growth rate (CAGR) of 2.8 percent from 2017 to 2022 with volumes forecasted to reach 1.68 billion units in 2022. Signaling its more cautious outlook, Hi-P guided to similar revenue but lower profit in FY18 as compared to FY17.

Internet Of Things

The Internet of Things (IoT) is the concept of connecting any device with certain functions to the Internet. It involves extending internet connectivity beyond standard devices to any range of traditionally non-internet-enabled physical devices and everyday objects.

On a smaller scale, the potential value towards an individual could be the automation of home appliances such as the switching on of lights and air conditioning when the individual is returning home from work.

On a broader scale, there are endless opportunities as cities could apply IoT to things like transportation networks, power and water supply systems. Benefits of such applications are huge as it can significantly reduce the man power required for various tasks and in turn result in cost savings. The IDC expects worldwide IoT spending to sustain a CAGR of 14.4 percent from 2017 to 2021, passing the US$1 trillion mark in 2020.

Given the immense potential of IoT, Hi-P has identified this as key growth driver in the future.

Potential Privatisation

Currently, Hi-P has a float of only 15.4 percent. Of the total outstanding shares, the largest single shareholder, Hsiao Tung Yao, holds around 83.4 percent.

The group renewed its latest share buyback mandate on 20 April 2018 and has since bought back a total of 3.7 million shares or 0.5 percent of the total outstanding shares. The share buyback mandate allows the group to purchase up to ten percent of the total number of issued shares, as of the date of the resolution passed by shareholders.

Assuming that the group purchases the maximum of ten percent, Hsiao’s ownership could potentially increase to around 92.6 percent, making it rather easy for a privatisation bid. In fact, the company will have to increase its free float or delist when the percentage reaches 90 percent.

Attractive Valuations

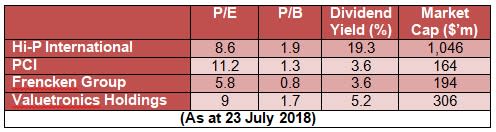

Despite the 40 percent gain since July last year, Hi-P’s shares are currently valued at a price-to-earnings (P/E) of 8.6 times, down from 9.8 times.

However, this does not imply that Hi-P’s shares at trading at a huge bargain at the moment, given the heightened geopolitical uncertainty leading to a decline in investor optimism.

Comparing the valuations of Hi-P against some of its peers provide a somewhat mixed picture. While Hi-P’s P/E remains comparable, the group’s shares are trading at almost double its price-to-book value.

Meanwhile, the most attractive factor for Hi-P is its dividend yield of 19.3 percent, the highest of all the SGX-listed companies. However, it is unlikely that Hi-P will pay out the same level of dividends this year as the high payout for FY17 far exceeded the group’s net earnings for the year.

Having said that, investors should trade with caution and not be misled by the high dividend yield as it is possible that part of the high payout for FY17 might be intended as a one-time distribution and should have been classified as special dividends instead.