Yahoo Finance

Yahoo Finance

SI Research: Fuel Your Returns With Union Gas Holdings

On the lookout for stable businesses whose products and services are always in demand, Union Gas Holdings (Union Gas) is one such company that caught our attention. Listed on the Singapore Exchange a couple of years back in July 2017 at $0.25 a share, Union Gas is a leading supplier of bottled Liquefied Petroleum Gas (LPG) cylinders to more than 180,000 domestic households in Singapore. People need to eat in order to survive, and in so doing they would require bottled LPG to cook their meals.

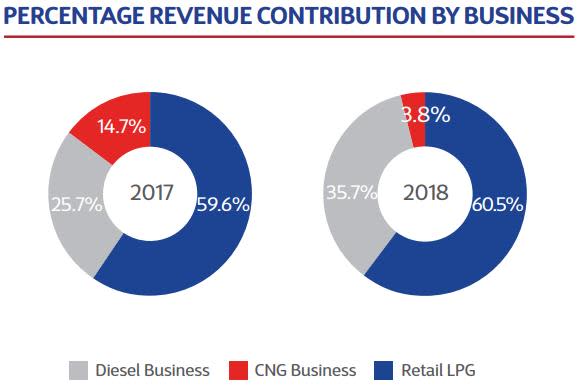

The retail distribution of bottled LPG cylinders and sale of LPG-related accessories make up a significant portion of Union Gas’s top-line at around 60.5 percent. Apart from its core LPG business, the group also sells and distributes diesel and compressed natural gas (CNG) to commercial and retail customers at its fuel station at 50 Old Toh Tuck Road, each contributing 35.7 percent and 3.8 percent of the remaining FY18 revenue respectively.

Source: Company Annual Reports

Acquisitions Spur Growth

Last year, Union Gas completed two notable acquisitions, namely U-Gas for a consideration of $9.2 million as well as Semgas Supply for $2.4 million. The former is primarily involved in the retail sale of LPG to hawker centres in Singapore, which would allow Union Gas to extend its sale of LPG to the commercial sector. As a result, this segment created a new revenue stream contributing an approximate $5.6 million to the group’s top-line in FY18.

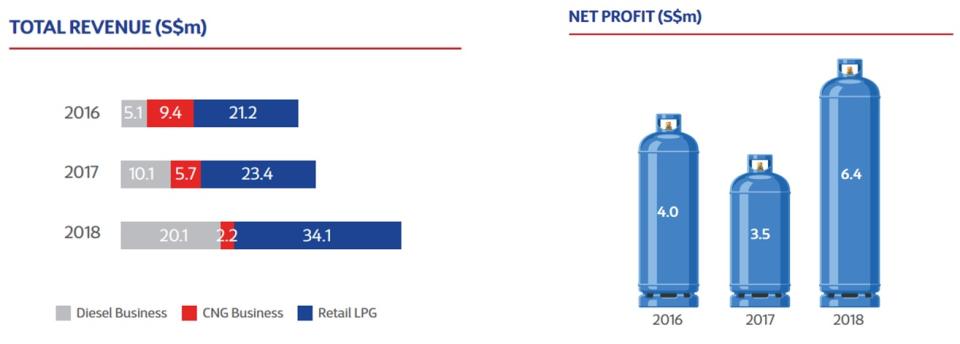

Meanwhile, the purchase of Semgas Supply, which has an average monthly historical volume of 13,748 LPG cylinders sold to domestic customers, also served to enlarge Union Gas’s domestic distribution network and strengthen its market share. Over the last three years, revenue from Union Gas’s retail LPG segment grew steadily at a compounded annual growth rate (CAGR) of 21.7 percent from $21.2 million in FY16 to $34.1 million in FY18.

Source: Company Annual Reports

Union Gas’ acquisitions in FY18 had clearly given a significant boost to the group’s top-line. Together with increased sales from the group’s diesel business which had almost doubled last year arising from higher oil prices and sales volume, FY18 revenue jumped 43.8 percent to $56.4 million. Correspondingly, net profit surged 84.9 percent to $6.4 million on the back of higher revenue over the same period.

Strong Cash Flows And Healthy Balance Sheet

Union Gas remained a strong cash generative business with net cash flow from operating activities in FY18 amounting to $8.4 million. In addition, the group’s balance sheet is also healthy with $15.7 million of cash versus $2.4 million of borrowings as at 31 December 2018, putting it in a strong net cash position of $13.3 million to execute future expansionary plans.

To share the fruits of a good year with its shareholders, Union Gas proposed a final dividend of $0.012 per share in FY18, which is equivalent to a healthy dividend payout ratio of around 42.8 percent of net profit. Based on the group’s last market price of $0.255 as at 22 April 2019, this implies an attractive dividend yield of 4.7 percent should the group continue to maintain similar payouts in subsequent years.

Long-Term Disruptions

That said, there are some trends with regard to Union Gas’ long-term prospects which although may not be immediately disruptive, but we feel are something that one should be mindful of.

Firstly, there has been a gradual shift in people’s eating and cooking habits. Newer homes today are connected with piped town gas which not only is more convenient with uninterrupted gas transmission, but also eliminates the need of storage space for LPG cylinders. According to data revealed by the Department of Statistics Singapore, total domestic piped gas sales grew steadily at a CAGR of 2.5 percent over the last twenty years from 464.6 million kilowatt hour (kWh) in 1998 to 761.5 million kWh in 2018. On the other hand, total LPG sales saw a gradual decline of negative 1.6 percent over the same period, from 124,697.9 tonnes in 1998 to 90,026.1 tonnes in 2018.

As families get smaller and dual-income households are becoming the norm, people tend to prefer to eat out more often instead of going through the hassles of preparing one’s own meals at home. Even if one has the leisure and time to cook, electric stoves today are quickly gaining popularity and seek to become a likely replacement for traditional fuel stove due to safety, ease of operation and maintenance considerations.

Once touted as the next big thing of green vehicles, CNG vehicles are now becoming a rare sight on the roads of Singapore with the advent of electric cars. Based on figures from the Land Transport Authority, CNG private car population has dwindled to about 1,000 in 2017 from the peak of 2,706 in 2010. The decline was even more drastic when it comes to CNG taxis after the last of CNG taxi owned by Trans-Cab has been scrapped in January 2018.

This had impacted Union Gas’ CNG segment adversely. Over the last three years, revenue from the group’s CNG business shrank at a CAGR of negative 51.6 percent from $9.4 million in FY16 to $2.2 million in FY18, as a result of decreased sales volume due to the declining number of natural gas vehicles operating in Singapore.

Last but not least, Union Gas currently purchases all of its bottled LPG cylinders from the UEC Group and is the third-party supplier of natural gas and diesel. This inadvertently subjects the group to the unpredictable fluctuations in purchase costs of bottled LPG cylinders, natural gas and diesel which in turn are largely dependent on the volatile crude oil prices.