Yahoo Finance

Yahoo Finance How Safe Are HCP and Its Dividend?

HCP (NYSE: HCP) is a healthcare real estate investment trust, or REIT, that primarily invests in three specific types of healthcare properties: medical offices, life science facilities, and senior housing properties. The company owns 776 properties, most of which can be classified into one of these three categories.

A much-improved healthcare REIT

In early 2016, HCP was not in great shape. It had a substantial portfolio of skilled-nursing facilities, and its primary tenant, HCR ManorCare, was facing extreme financial difficulty. Plus, HCP's senior housing portfolio was highly leveraged to a single tenant, Brookdale Senior Living (NYSE: BKD), and the company's balance sheet wasn't exactly stellar.

Image Source: Getty Images.

Since that time, HCP has undergone a multiyear transformation that has resulted in a much more sustainable and healthy business. To name just a few of the steps that have been completed:

HCP spun off its skilled nursing assets into a newly created REIT called QCP, which has since been acquired.

HCP sold a substantial amount of its Brookdale-occupied properties and transitioned 35 others to new operators. Now HCP's Brookdale exposure has fallen from 34% of its income to 16%.

HCP exited several other noncore investments or is in the process of doing so -- such as its U.K. portfolio. A 51% stake in the U.K. assets has already been sold, and the rest is expected to be disposed of in 2019.

HCP paid down some of its debt. Its net debt to adjusted EBITDA has dropped from 6.5 to a pro forma 6.0.

HCP now has a high-quality portfolio of healthcare assets, most of which (95%) derive their revenue from predictable private-pay sources. The company's income isn't too dependent on any single tenant, and its improved balance sheet gives it ample liquidity to pursue opportunities as they arise.

In fact, because of the company's balance sheet improvements and higher asset quality, S&P recently upgraded HCP's credit rating from a BBB to a BBB+. This was one of HCP's stated goals when it started its transformation process a few years ago and is a very positive sign that the process has been a success.

Now HCP is ready to ramp up its spending on development projects and acquisitions. The company expects to increase its development spending from $240 million in 2017 to $300 million to $400 million per year for the next several years.

Big demographic tailwinds and room for consolidation

There are two major reasons to love healthcare real estate, and HCP in particular, as a long-term investment.

First, there are favorable demographic tailwinds that should keep demand for healthcare real estate high. As the massive baby boomer generation ages, the senior citizen population is expected to explode, which should be a positive catalyst for all three of HCP's core property types.

The 65-and-over population in the U.S. is expected to grow by 19% by 2030, and the oldest subsets of this group are going to grow even faster. Simply put, seniors utilize healthcare facilities more than younger people do. In fact, the average American over 65 visits medical facilities 6.6 times per year -- 144% more than the average person under 45.

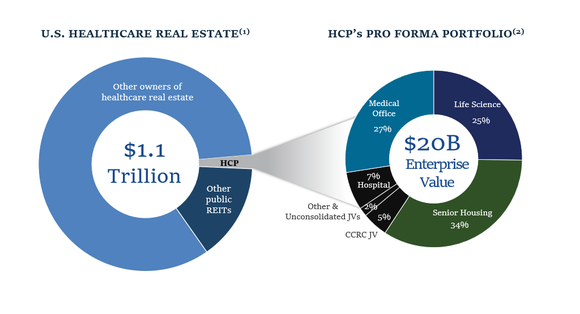

In addition to the demographic tailwinds, there's a tremendous opportunity for consolidation in the existing healthcare real estate market. There is roughly $1.1 trillion worth of healthcare real estate in existence right now, and only about 15% of this is REIT owned. In contrast, many other forms of commercial real estate such as hotels and malls are 40% REIT owned or more.

Image Source: HCP investor presentation.

This is especially true when it comes to medical offices, a core component of HCP's portfolio. These properties have a disproportionally high ownership rate by physicians, health systems, and private investors. So not only is there likely to be steady demand growth in the years ahead, but there is an addressable opportunity in the hundreds of billions of dollars already invested.

Are the stock and its dividend safe?

In a nutshell, yes. HCP currently pays a dividend of $1.48 per year in quarterly installments. With expected adjusted FFO (the REIT version of earnings) in the range of $1.79 to $1.83 for 2018, HCP's dividend is well covered by its income. And with its transformation plan finally nearing completion and a massive long-tailed market opportunity ahead, HCP should be a strong and safe performer for years to come.

More From The Motley Fool

Matthew Frankel, CFP owns shares of HCP. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.