Yahoo Finance

Yahoo Finance Reasons to Add Quest Diagnostics (DGX) Stock to Your Portfolio

Quest Diagnostics Incorporated DGX has been gaining on the back of its improvements in its base volumes. The optimism led by solid fourth-quarter 2022 performance and its tactical approaches to accelerate growth also buoy optimism. Headwinds resulting from stiff competition and a soft volume environment are major downsides.

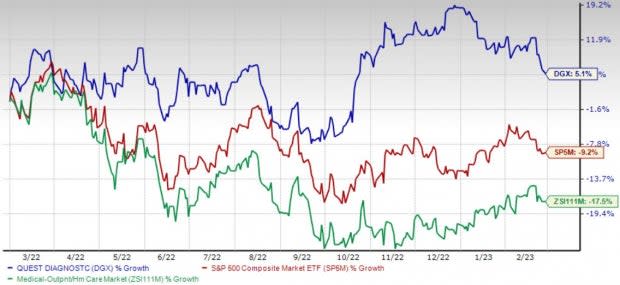

Over the past year, the Zacks Rank #2 (Buy) stock has gained 5.1% against the 17.5% decline of the industry and the 9.2% fall of the S&P 500.

The renowned provider of diagnostic information services has a market capitalization of $15.44 billion. The company projects 2.4% growth for 2024 and expects to witness continued improvements in its business. Quest Diagnostics surpassed the Zacks Consensus Estimates in all the trailing four quarters, delivering an earnings surprise of 7%, on average.

Image Source: Zacks Investment Research

Let’s delve deeper.

Base Volume Improves: We are optimistic about Quest Diagnostics’ base testing volumes or base business, which refers to testing volumes excluding COVID-19 testing. The company is increasing its efforts to drive productivity and expand margins in the base business. Quest Diagnostics continued to drive additional productivity improvements with lab platform consolidation and greater use of automation and artificial intelligence in the fourth quarter of 2022.

Accelerate Growth Strategy Bodes Well: Quest Diagnostics continues to progress in terms of its tactical approaches to accelerate growth, the first part of its two-point strategy, raising our optimism. In terms of growth through M&A, the company has announced an outreach lab purchase from Ohio-based Summa Health. Quest Diagnostics has also announced a professional lab services relationship with Southwest Florida-based Lee Health to provide supply-chain expertise for five hospitals owned by Lee Health and selected outpatient centers.

To accelerate growth through health plan access, the company continued to gain traction with value-based contracts, where it sees higher growth than traditional contracts.

Strong Q4 Results: Quest Diagnostics’ better-than-expected fourth-quarter 2022 earnings and revenues buoy our optimism. During the reported quarter, the base business registered growth and the company has also ramped up investments to accelerate growth in the base business, particularly in the areas of advanced diagnostics and direct-to-consumer testing.

Downsides

Stiff Competition: Quest Diagnostics faces intense competition, primarily from other commercial laboratories and hospitals. Hospitals control an estimated 60% of the diagnostic test market, compared to Quest Diagnostic’s 15% share. While pricing is an important factor in choosing a testing lab, hospital-affiliated physicians expect a high level of service, including the accurate and rapid turnaround of testing results. As a result, Quest Diagnostics and other commercial labs compete with hospital-affiliated labs primarily based on the quality of service.

Soft Volume Environment: Pressure on volume, owing to a difficult macroeconomic situation and pricing, constitutes the primary risk for Quest Diagnostics. Total volume, measured by the number of requisitions, was down 11.2% year over year in the fourth quarter. Revenues per requisition declined 5.1% year over year due to lower COVID-19 molecular testing volume.

Estimate Trend

Quest Diagnostics has been witnessing a positive estimate revision trend for 2023. In the past 90 days, the Zacks Consensus Estimate for its earnings per share has moved 2.7% north to $8.69.

The Zacks Consensus Estimate for first-quarter 2023 revenues is pegged at $2.20 billion, suggesting a 15.6% decline from the year-ago reported number.

This compares to our first-quarter 2023 revenue estimate of $2.20 billion, suggesting a 15.7% plunge from the year-ago quarter’s reported number.

Other Key Picks

A few other top-ranked stocks in the broader medical space are Hologic, Inc. HOLX, McKesson Corporation MCK and Avanos Medical, Inc. AVNS.

Hologic, sporting a Zacks Rank #1 (Strong Buy) at present, has an estimated long-term growth rate of 15.2%. HOLX’s earnings surpassed the Zacks Consensus Estimate in all the trailing four quarters, the average beat being 30.6%. You can see the complete list of today’s Zacks #1 Rank stocks here.

Hologic has gained 13.3% against the industry’s 14.7% decline in the past year.

McKesson, carrying a Zacks Rank #2 at present, has an estimated long-term growth rate of 10.4%. MCK’s earnings surpassed estimates in two of the trailing four quarters and missed the same in the other two, the average beat being 3.4%.

McKesson has gained 30.8% against the industry’s 8.2% decline over the past year.

Avanos, carrying a Zacks Rank #2 at present, has an estimated growth rate of 1.8% for 2023. AVNS’ earnings surpassed estimates in all the trailing four quarters, the average beat being 11%.

Avanos has lost 19.1% compared with the industry’s 14.7% decline over the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Quest Diagnostics Incorporated (DGX) : Free Stock Analysis Report

McKesson Corporation (MCK) : Free Stock Analysis Report

Hologic, Inc. (HOLX) : Free Stock Analysis Report

AVANOS MEDICAL, INC. (AVNS) : Free Stock Analysis Report