Yahoo Finance

Yahoo Finance Linc Energy Ltd - Can the Blair Athol Mine keep going for more than three years?

31/1/2014 – Before it listed on the Singapore Exchange in December last year, Linc Energy Ltd produced the largest offer document we've ever come across: 1,572 pages in six parts, which are compiled into two volumes.

The purpose of prospectuses is to enable investors to make an informed decision before buying shares.

While Linc certainly fulfilled its obligations, as far as we're concerned such a voluminous document defeats the purpose.

Linc Energy was originally listed on ASX in May 2006, and in the years since then was sometimes in the news for all the wrong reasons.

According to a report in Melbourne's The Age newspaper in April 2011, convicted drug dealer Tony Mokbel, with the help of associates, bought shares in Linc Energy with "dirty money".

In fact, the police allege Tony Mokbel had a meeting with Linc Energy's controlling shareholder and CEO Peter Bond.

Later, Tony Mokbel was convicted and is presently serving a 30-year jail term, reportsThe Age.

In recent years, Linc Energy's shareholders have strongly opposed the generous pay packages of its executives.

Its shareholders protested against the executive remuneration report for the last three consecutive years.

The "two-strikes" rule in Australia empowers shareholders to call for a vote on the board of directors if more than 25% shareholders vote against the remuneration report for two years in a row.

However, Linc Energy's controlling shareholder and CEO Peter Bond managed to avoid a board "spill" in November 2012.

In spite of that, Linc Energy couldn't avoid a third strike in November last year.

Though Linc Energy hired PriceWaterhouseCoopers after the first strike in 2011 to redesign the reward structure of its executives, the fixed remuneration of Mr Bond has doubled in the past three years.

Despite its colourful past, the IPO of Linc Energy on SGX seems to be a hit.

Listing at an offer price of S$1.20/share on December 18, Linc Energy's stock price has run up more than 25% since then.

But after taking up the daunting task of reading the prospectus, we have a long list of questions that need to be asked.

First, Linc Energy issued 47.85 mln shares to Genting Berhad in the IPO, which is twice the total shares on offer.

It seems Genting Berhad bought some of its stake from the existing shareholder(s) of Linc Energy but we can't find where in the prospectus it clarifies that.

Also, Linc Energy has given Genting Berhad the option to buy another 10.75 mln more shares at the IPO price within six months of listing.

Second, Linc Energy's offer statistics don't add up for us.

For instance, the total number of shares issued are about twice what was mentioned in the prospectus.

And due to that, the total funds raised in the IPO don't add up for us.

Third, Linc Energy's Umiat oil field seems overvalued in the prospectus, after taking into account the independent valuer's comments in its FY13 annual report.

Fourth, the 'qualified persons' apparently didn't visit its oil and gas assets, and prepared their reports only on the basis of information provided by Linc Energy.

Fifth, Linc Energy is involved in a tax dispute in Australia and it has not yet made any provisions for an adverse outcome.

Sixth, Linc Energy's CEO has agreed to lend some of his shares to Credit Suisse Europe, and such shares are not subject to the lock-in period.

Seventh, we can't find where the company declared the cost of acquiring the Blair Athol Mine, while the expected life of the mine seems very long indeed.

These are some of the 51 questions asked in this report.

We have sent these questions to the company to invite them for an on-camera interview, and/or seek their written response.

Janelle van de Velde, President Corporate Services replied: "Thank you for your email sent to our generic email address. Please note that our CEO is currently on leave, returning on 3rd February however in the meantime, we will be reviewing your questions with the intention of responding as soon as Mr Bond has returned to the office."

We will update this story in the hopeful event we receive a reply.

BACKGROUND

Linc Energy Ltd was incorporated in October 1996 as a no liability public company under the name 'Linc Energy NL'.

In November 2000, it was converted into a public company limited by shares. That's when it assumed its present name.

It was listed on the Australian Securities Exchange and once counted the Premier of the state of Queensland, Mike Ahern, on its board.

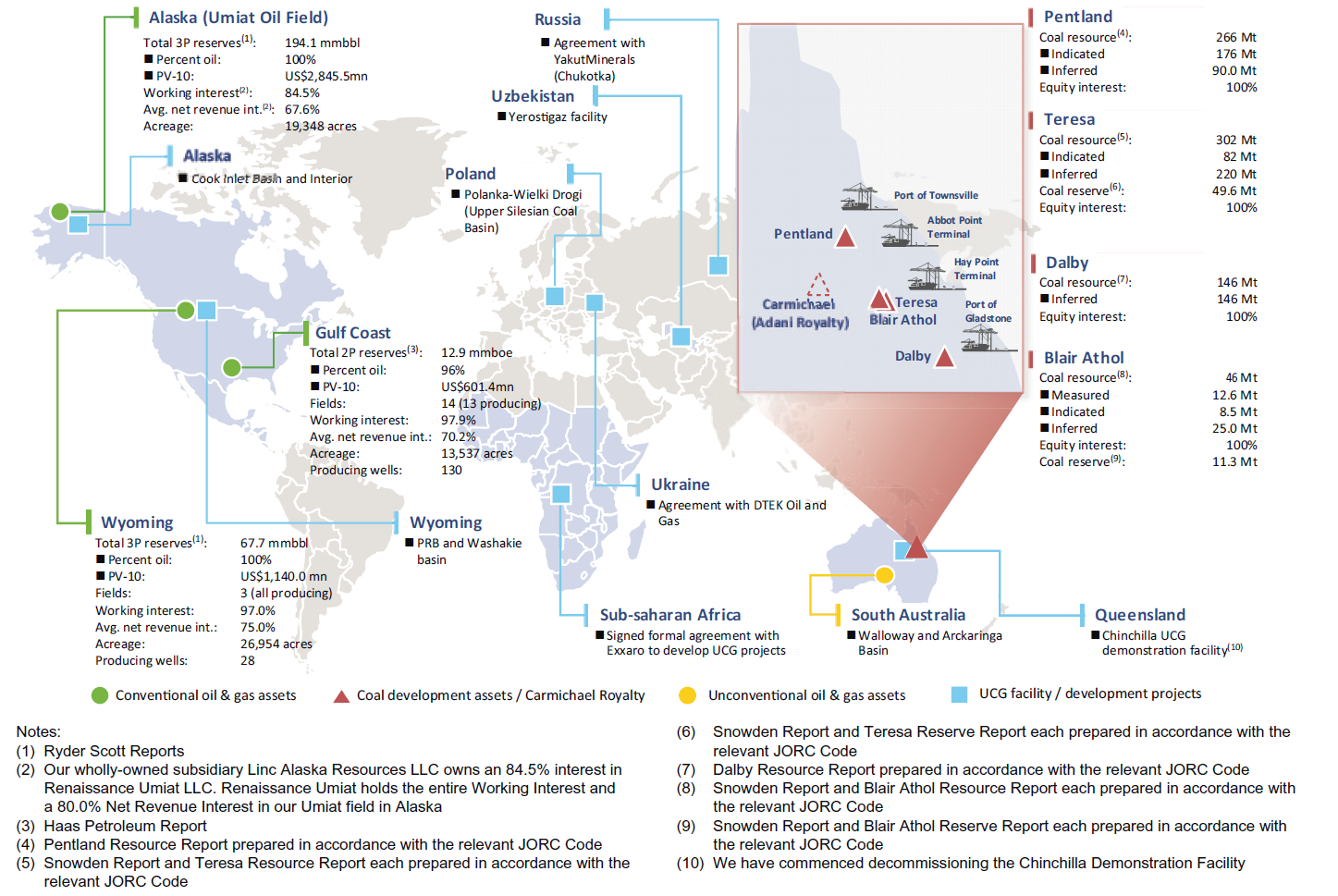

Linc Energy has conventional oil and gas assets in three regions in the US.

It owns oil producing fields in the Gulf Coast Region and the state of Wyoming, which generate the majority of its revenue.

The company is also developing the Umiat Oil Field, acquired in July 2011, in the state of Alaska.

Linc Energy also indulges in the unconventional oil and gas business.

The company's clean energy business focuses on commercialisation of its patented Underground Coal Gasification (UCG) to Gas-to-Liquid (GTL) technology.

Linc Energy says its Chinchilla Demonstration Facility in Queensland, Australia is the only UCG to GTL facility in the world.

Linc Energy also owns and operates the world's longest running commercial UCG project in Angren, Uzbekistan.

It owns a 91.3% stake in the project which has been operating for over five decades and supplies energy to the Angren power plant.

Linc Energy also owns coal interests for UCG in the states of Wyoming and Alaska in the US, Poland, Uzbekistan, and Queensland and certain southern regions in Australia.

Linc Energy's unconventional oil and gas business also includes exploration of shale oil and gas in the Arckaringa Basin which is spread over an area of 65,000 sq km in South Australia.

Apart from the conventional and unconventional oil and gas business, Linc Energy holds coal assets.

The company is entitled to a royalty of A$2 per tonne over a period of 20 years from the Carmichael Coal Tenement it sold for A$500 mln in 2010.

Linc Energy also owns conventional coal mining assets in Queensland, Australia.

In October 2013, it acquired the Blair Athol Coal Mine in Australia at an undisclosed price from Rio Tinto.

As on September 1 last year, Linc Energy estimated its conventional oil and gas assets hold 'proved' oil and gas reserves (also called 1P reserves) of 13.6 MMBOE, of which 96% was oil, with an estimated net present value (at 10% discount rate on future cash flows) of US$614.5 mln.

More than 90% of its 'proved' reserves were contributed by the producing oil and gas assets in the Gulf Coast Region in the US.

And the remaining 'proved' reserves came from the producing oil and gas assets in Wyoming.

Linc Energy had 'proved plus probable' oil and gas reserves (also called 2P reserves) of 168.2 MMBOE with an estimated net present value of US$3.1 bln.

Finally, Linc Energy's 'proved plus probable plus possible' oil and gas reserves (also called 3P reserves) stood at 274.6 MMBOE with an estimated net present value of US$4.6 bln.

Linc Energy Ltd first listed on the Australian Stock Exchange in May 2006.

In this video, Linc Energy's CEO explains why the company wanted to migrate to the SGX.

With its successful listing on the SGX in December last year, the company delisted its shares from the Australian Securities Exchange.

Further details can be found on page 116 of the prospectus.

Investor Central. Asian insights for global investors. We ask the tough questions of Asian companies which global investors need answers to.

FINANCIALS

The company has disclosed these results for the most recent financial year ended June 30, 2013:

Revenue: +118% to A$124.4 mln

Profit: (A$63.8 mln) vs (A$61.9 mln)

Impairment of oil and gas assets and financial assets: (A$23.5 mln) vs Nil

Net fair value gain on convertible notes: A$19.7 mln vs Nil

Cash flow from operations: (A$5.7 mln) vs (A$85.9 mln)

Dividend: Nil

Order book: Not maintained

Linc Energy sold Carmichael coal tenement to Adani Mining Pty Ltd for A$500 mln (US$466.8 mln) cash in August 2010 (refer page 10).

Adani Mining would also pay Linc Energy a royalty of A$2 per tonne in the first 20 years of production at the Carmichael mine project in Queensland, Australia.

According to page 36, Linc Energy is involved in discussions with the Australian Taxation Office regarding tax treatment on the prospective royalty income.

Adani Mining is expected to commence production at the Carmichael mine project in 2017.

Therefore Linc Energy will receive royalty payments from 2017 onwards.

But the Australian Tax Office (ATO) formed a preliminary view in October 2013 that the market value of the royalty deed between Linc Energy and Adani Mining should be taxable in FY11.

As a result, the ATO decided to commence an audit.

Linc Energy says it has legal and tax advice to support its stand in the FY2011 tax return lodged with the ATO that the value of the future amounts receivable under the deed should not be taxable upfront, but rather assessed on receipt over 20 years from 2017.

So far, Linc Energy has not made any provision for the resultant tax liability.

According to Linc Energy's Q1 FY14 earnings report (page 3), Adani Mining is looking to ramp up the full production at the Carmichael mine project to 60 million tonnes per annum by 2023.

Apparently, the royalty income of Linc Energy for a period of 20 years would be pretty significant.

1. How much tax on royalty deed will Linc Energy have to pay. What is the worst case scenario?

The prospectus didn't mention how much tax the ATO was demanding from Linc Energy for FY2011.

The company has not made any provision for that so far.

But now that it is aware of the preliminary view of the ATO, would Linc Energy do it now?

It would be fair to say that the tax liability could be in the millions because the royalty income over a 20 year period might add up to be more than a billion dollars.

Certainly, a tax liability on the royalty deed would push Linc Energy further into the red and might also strain the covenants of its debt arrangements.

2. How likely is the Uzbekistan government to buy "golden shares" in Yerostigaz?

Linc Energy owns a 91.6% stake in Joint Stock Company Yerostigaz in Uzbekistan.

The remaining 8.4% stake is owned by the management of Yerostigaz.

According to page 115, as per the Uzbekistan Company Law, the Cabinet of Ministers of the Republic of Uzbekistan may introduce special rights in the form of "Golden Shares" to participate in and manage certain joint stock companies in which the government has less than a 25% stake.

Yerostigaz JSC owns the world's longest running commercial UCG project which has been operating for over five decades and supplies energy to the Angren power plant in Uzbekistan.

Linc Energy recorded A$2.3 mln in revenue from the sale of UCG syngas in Uzbekistan (pages 75 & 87).

Therefore that makes us curious about the likelihood of the government exercising its special rights in the case of Linc Energy's subsidiary.

Further details can be found on page 71 of the prospectus.

GROWTH DRIVERS

Ramping up oil production

Linc Energy's oil fields in the US were producing an average of 5,858 barrels of oil equivalent per day (BOEPD) between October 1 and November 15 last year (refer page 121).

It had a target of increasing the production at the wells in the Gulf Coast Region to 8,000 to 9,000 BOEPD before December 31 last year.

3. Did it achieve the targeted production of 8,000 to 9,000 BOEPD in the Gulf Coast Region in December?

Further, at the time of the IPO, the company had identified a portfolio of about 60 prospects in the Gulf Coast Region, to drill for sub-salt oil and gas in the next two years.

In Alaska, Linc Energy estimates a capital expenditure of US$1.8 bln and operating expenditure of US$589 mln at its Umiat field, to target a peak production of 50,000 barrels of oil per day (BOPD) before 2020.

In Wyoming, Linc Energy plans to ramp up the production to 10,000 to 15,000 BOPD in the next three to five years provided, it manages to procure adequate supply of carbon dioxide at the sites.

Shale Gas exploration at Arckaringa Basin in South Australia

Linc Energy says, based on DeGolyer and MacNaughton report, Arckaringa Basin's 'risked mean prospective resources' include 516 MMBBL of oil, 9.9 TCF of gas and 1,263 MMBL of condensate (page 149).

According to Degolyer and MacNaughton's report on page I-358 in Volume Two of the prospectus, the prospective resources estimated by them are those quantities of petroleum that are potentially recoverable from accumulations yet to be discovered at the Arckaringa Basin in South Australia.

It adds, because of the uncertainty of commerciality and the lack of sufficient exploration drilling, the prospective resources estimated in the report cannot be classified as contingent resources or reserves.

In simple words, the prospective resources mentioned in the prospectus are not reliable enough to judge the commercial worth of the oil and gas in the Arckaringa Basin.

In fact, on page 149, the prospectus says "there is no certainty that any portion of the prospective resources estimated herein will be discovered. If discovered, there is no certainty that it will be commercially viable to produce any portion of the prospective resources evaluated".

4. How much investment would it take to explore and exploit the Arckaringa Basin?

To impress the investors, companies often disclose massive reserves of undeveloped assets.

But the real test lies in the commercialisation of those assets.

Therefore, how much would Linc Energy have to invest in capital and operational expenditure to extract the possible reserves?

Commercialisation of UCG Technology

Linc Energy has invested about A$210 mln (US$196 mln) in the UCG technology in the last nine years (refer page 122).

Underground coal gasification (UCG) is the process of creating synthetic natural gas out of coal, while it is still underground, by setting it on fire and injecting it with oxygen and water.

According to an article on thinkprogress.org, the local residents and environmental groups in Wyoming are protesting against Linc Energy's proposed UCG project.

It is alleged that UCG is an untested process which contaminates the nearby water deposits with deadly Benzene.

The matter was heard by the Wyoming Environmental Quality Council which subsequently ruled in favour of Linc Energy.

It is worth pointing out here that Linc Energy had to decommission its Chinchilla Demonstration Facility in Queensland, Australia after the Department of Environment and Heritage Protection (DEHP) served a notice regarding an unlawful release of contaminants from the facility.

You can read more on it in the 'Ongoing Litigation' section later in this story.

5. Can Linc Energy commercialise its UCG Technology?

As of today, Linc Energy's UCG Technology has not been put to commercial use.

Therefore it remains to be seen if it can do so profitably in the future.

On November 30, 2012, Linc Energy signed an agreement with DTEK Holdings Ltd for the collaboration and evaluation of the UCG potential in Ukraine in relation to DTEK Holdings' local coal resources (page 147).

DTEK Holdings has agreed to pay Linc Energy for an initial resource assessment.

6. How much did/will DTEK Holdings pay Linc Energy for the initial assessment study?

If a coal resource suitable for UCG commercialisation is identified, both the companies will co-operate to bring a UCG gas project in Ukraine.

In yet another collaboration last year, on May 30, Linc Energy entered into an agreement with Exxaro Resources to pursue energy solutions business in Sub-Saharan Africa (page 146).

According to the agreement, Exxaro Resources has a non-exclusive right to use Linc Energy's UCG Technology in Sub-Saharan Africa, for a total licence fee of A$30 mln (US$28 mln).

Of that, Exxaro Resources has paid A$3 mln (US$2.8 mln) on signing of the initial term sheet.

The next payment of A$20 mln (US$18.7 mln) will be made once all the conditions in the agreement are satisfied.

As on November 15 last year, only one of such conditions, which relates to the extension of prospecting rights over the current area of interest for this project, remained outstanding.

The balance of A$7 mln (US$6.5 mln) is payable on the completion of the performance testing of the first project, which is currently targeted for 2017.

In addition to the licence fees, Linc Energy will receive a royalty for the UCG syngas produced and sold from the project.

Linc Energy will also provide engineering services to the joint venture as per the licence agreement.

The bankable feasibility study to support the initial project is estimated to be completed by mid-2015, with commissioning of the first gasifier scheduled in mid-2016.

Linc Energy will hold a minimum 15% equity interest in the project and has an option to raise it to a 49% equity interest in this, as well as all subsequent UCG projects which Exxaro Resources develops.

On June 19 last year, Linc Energy signed a letter of intent and services agreement with LLC Yakut Minerals, an affiliate of Ervington Investments Ltd, to assess the potential of deploying UCG technology on the coal resources at Chukotka in North Eastern Russia (page 146).

Linc Energy also plans to leverage on its UCG technology through joint ventures with strategic partners within the Asian region especially, in China, Mongolia and Indonesia (page 125).

Proposed divestment/demerger of coal assets

In an announcement on ASX on November 13, Linc Energy revealed its plan to demerge/divest its coal assets held through wholly-owned subsidiary New Emerald Coal.

In that announcement, Linc Energy estimated its coal assets to be worth A$440 mln.

The company plans to divest the coal assets so that it can focus on its core conventional and non-conventional energy business.

Linc Energy has proposed the divestment/demerger of New Emerald Coal during 2014.

The company's major coal assets include the Teresa Project and the recently acquired Blair Athol Mine in Australia.

Undisclosed costs related to recently acquired Blair Athol Coal Mine

In October last year, Linc Energy's wholly-owned subsidiary New Emerald Coal Ltd acquired the Blair Athol Coal Mine from a joint venture controlled by Rio Tinto in Queensland, Australia.

In its announcement on October 3, Linc Energy said 'no upfront cost' was associated for the acquisition of Blair Athol Mine.

But on page 84 of the prospectus, it says the acquisition was made at a nominal amount, financed from its internal funds.

That begs the question:

7. How much did it pay to acquire the Blair Athol Mine?

Linc Energy has assumed all the rehabilitation liabilities associated with the mine and it will receive fixed cash compensation over a period of years from the vendor to meet its rehabilitation obligations.

On page 54, the prospectus highlights that Linc Energy will have to provide up to A$90 mln (US$84 mln) towards environmental rehabilitation bonds in order to recommence production at the Blair Athol Mine.

Blair Athol Mine was closed in November 2012 as the Rio Tinto led joint venture decided not to extend the life of the mine, which had been in operation for about 30 years.

According to a report in the Wall Street Journal, Rio Tinto estimates at least 10 million metric tonnes of coal is still left at the mine.

In the prospectus, the independent qualified persons' report also estimates total marketable coal reserves of 9.5 million tons (refer page I-603 of Volume Two).

In its October 3 announcement, Linc Energy said it planned to recommence the production at the mine in 2014, with the aim of producing 3 million tonnes of coal every year.

At that pace, the mine would stay in production for three to four years.

In that announcement Linc Energy also revealed the statutory site rehabilitation at the Blair Athol Mine will commence in 2016 and end in 2019.

Therefore Linc Energy has about 3 years to extract coal from the mine before it goes into rehabilitation.

But before that, the lease of the Blair Athol Mine would be due for renewal on November 30 later this year.

Taking into account all these risks, it seems to be a tightrope for Linc Energy to recommence the production at the Mine.

Curious independent valuation of Blair Athol Coal Mine

On page 166, the prospectus highlights the reserves and discounted cash flow valuation of Linc Energy's coal mines.

Based on 'Independent Qualified Person's report' prepared by Snowden Mining Industry Consultants Pty Ltd, the Blair Athol Mine is said to have proved and probable reserves of 11.3 million tonnes and a discounted cash flow valuation of A$181 mln.

The complete report prepared by Snowden Mining is appended in 'Volume Two' of the prospectus.

8. Why did Snowden Mining add 8.7 million tonnes above the JORC-compliant proved and probable reserves of the Blair Athol coal mine?

According to page I-628, Snowden Mining estimated the marketable coal reserves at the Blair Athol Mine to be 9.5 million tonnes.

But in the 'Life of Mine Plan', Snowden Mining has added 8.7 million tonnes above the JORC-compliant proved and probable reserves of the coal mine.

Snowden Mining says the 8.7 million tonnes of coal is expected to be delivered from the partial block extraction (PBE) system of mining and it has been estimated from the 'inferred resources' of the coal mine which is why it has not been included in 'coal reserves' of Blair Athol Mine.

In simple words, the independent qualified person has included 8.7 million tonnes of 'inferred resources' of coal while calculating the life and production of Blair Athol Mine.

But according to JORC 2012 guidelines (page 12), 'inferred mineral resources', by definition, are not expected to be upgraded to 'probable reserves'.

Therefore it seems odd that Snowden Mining included 'inferred resources' while determining the production life of Blair Athol Mine.

This is critical, because this coal production estimate is the basis for Snowden Mining's calculated cash flow at the Mine for a period of 10 years up to 2025.

Apart from the estimated coal production, a few other things don't fit in with the independent qualified person's estimate.

9. On what basis did Snowden Mining assume that the lease of Blair Athol Mine will be renewed?

First, the lease of Blair Athol Mine is due to expire in November 2014.

It seems to be an assumption by Snowden Mining that the lease will be renewed by the authorities, given that the mandatory rehabilitation is yet to be completed.

10. Can the mine undergo rehabilitation alongside being in production?

Second, the Blair Athol Mine is scheduled to undergo a statutory rehabilitation from 2016 to 2019.

It is not clear if the Mine can be in production and undergo rehabilitation at the same time.

11. How could Snowden Mining estimate the cash flows over a period of 10 years?

Third, even Rio Tinto, the controlling partner of the vendor joint venture, estimated the Blair Athol Mine to contain 'measured resources' of 10 million tonnes and 'indicated resources' of 0.2 million tons in its 2012 annual report (refer page I-560).

After having operated the Mine for about three decades, it seems highly unlikely that Rio Tinto would have not had a fair estimate of the reserves at the time of selling it to Linc Energy.

Finally, at an annual production rate of 3 million tonnes, the Blair Athol Mine will be exhausted in about three years.

Then, how could Snowden Mining estimate the cash flows over a period of 10 years?

Snowden Mining's Reply:Thank you for your inquiry in regards to Snowden's involvement with Linc Energy. As a consulting company, Snowden are under a strict confidentially agreement and we are trusted by our clients to not disclose any information without their consent. As such we are unable to comment on any projects that we work on. We are sorry we are unable to help you with your request but we ask you to respect our decision as our company's reputation is built on the trust of our clients. For any further questions or enquiries please contact Linc Energy directly.

12. What is the true value of its Blair Athol Coal Mine?

Having read the assumptions of Snowden Mining's valuation report, it is difficult to accept that the Blair Athol Mine is indeed worth A$181 mln.

Any reasonable investor would now wonder what could be a reliable valuation of the Mine.

13. Is the CEO sure about his numbers?

In an announcement on November 13, Mr Peter Bond said: "It's worth noting that the upgrade in coal resource at the Blair Athol mine should allow for a ten year mine life at a production rate of 3 million tonnes per annum".

In that announcement, Linc Energy revealed that Blair Athol Mine had a JORC resource of 46 million tonnes of coal of which, 12.6 million tonnes was 'measured', 8.5 million tonnes was 'indicated' and 25 million tonnes was 'inferred'.

According to Mr Bond's statement, the Blair Athol Mine would produce 30 million tonnes of coal over a decade.

But Snowden Mining's report clearly states the marketable coal reserves are about 9.5 million tonnes.

Therefore it is difficult to understand the basis on which Mr Bond estimated 30 million tonnes of production over a decade.

(Total number of questions in the full story: 51)

About Investor Central

We are an award-winning, tailored news service that dares to ask the questions that need to be asked.

We only report on companies our subscribers have selected in their watch lists, so start your own watch list now.

While our purpose is to ask the questions which the man on the street would ask, and to help the everyday investor make informed investments, please note that:

Our articles and presentations ('our contents') are not investment advice nor should they be construed as investment advice or any recommendation of any kind; nor meant to cast allegations or insinuations of any kind against any individuals or entities. Before acting on the material in our contents, you should either seek independent advice tailored to your particular circumstances and intentions or rely on your own judgement.

Our articles and presentations express our observations, opinions and theoretical analysis based on the facts that we have gathered or have been provided to us. While we endeavour to ensure that our contents are accurate and are presented in good faith, we cannot and do not warrant the accuracy, adequacy or completeness of the material or that the material is suitable for its intended use; and we disclaim any such warranties express or implied that may be presumed by any party; neither do we take responsibility for the views of companies or other stakeholders or observers or sources quoted or hyperlinked in our contents. While every precaution has been taken in the preparation of our contents, we (and our principals) shall not be liable for any losses or damage or inconveniences due allegedly to errors or omissions in any facts or due allegedly to reliance on our contents in any way whatsoever; nor for any damage to any computer hardware, date information or materials allegedly caused by our contents.

All expressions of opinion and observations in our contents are subject to change without notice and we do not undertake a duty to update and supplement our contents or the information contained herein in the event we obtain any further or more complete information.

©2014 Investor Central® - a service of Hong Bao Media