Yahoo Finance

Yahoo Finance Factors Likely to Decide Boot Barn's (BOOT) Fate in Q3 Earnings

Boot Barn Holdings, Inc. BOOT is likely to see top- and bottom-line improvement when it reports third-quarter fiscal 2022 earnings results. The Zacks Consensus Estimate for its quarterly revenues is pegged at $485.9 million, indicating an improvement of almost 60.7% from the year-ago figure.

The Zacks Consensus Estimate for earnings currently stands at $2.25, which suggests a sharp jump from earnings of $1.00 per share reported in the year-ago period. The consensus mark has increased 3.7% in the past seven days.

The Irvine, CA-based lifestyle retailer of western and work-related footwear, apparel and accessories has a trailing four-quarter earnings surprise of 35.3%, on average. In the last reported quarter, the company’s bottom line outperformed the Zacks Consensus Estimate by a margin of 29.8%.

Key Factors to Note

Boot Barn has been successfully navigating through the challenging environment, courtesy of merchandising strategies, omni-channel capabilities and better expense management as well as marketing. This, combined with the expansion of the store base has helped it gain market share, and in turn revenues.

Amid the pandemic, the company’s e-commerce business has been strong. Management has been boosting the omni-channel offerings to enhance customers’ experience through buy online pickup in-store, buy online curbside pickup, in-store fulfillment, same-day delivery, and buy online return in-store.

It has been witnessing robust merchandise margin driven by improved full-price selling and growth in exclusive brand penetration. It has been seeing strength in categories like work boots, men's and ladies’ western apparel, men's and ladies’ western boots, hats and non-flame resistant work apparel.

While the aforesaid factors boost optimism, ongoing supply chain issues and rising freight costs remain concerns. Also, any increase in operating expenses due to higher store payroll and overhead might get reflected in the to-be-reported quarter’s margins.

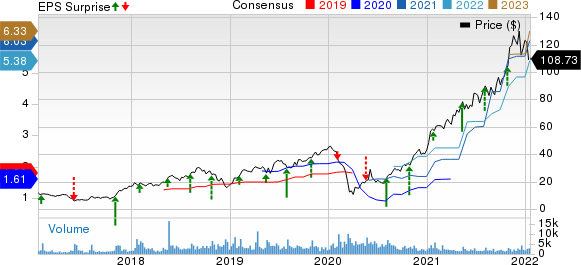

Boot Barn Holdings, Inc. Price, Consensus and EPS Surprise

Boot Barn Holdings, Inc. price-consensus-eps-surprise-chart | Boot Barn Holdings, Inc. Quote

Preliminary Q3 Results

Boot Barn reported preliminary third-quarter numbers on Jan 7, 2022. The company highlighted that net sales for the third quarter ended Dec 25, 2021 surged 71.1% to about $485.9 million compared with the quarter ended Dec 28, 2019. Impressively, same store sales jumped approximately 61%, reflecting an increase of 59.1% and 69.3% in retail store same store sales and e-commerce sales, respectively. Excluding the tax benefit, earnings per share for the quarter under discussion soared 175% to $2.23 from 81 cents in the quarter ended Dec 28, 2019.

Better team execution and ongoing customer growth contributed to the outstanding sales performance. Boot Barn even managed to maintain a strong inventory position and hire enough seasonal workers in spite of lingering supply chain woes and labor challenges. Management also stated that merchandise margin expanded 420 basis points compared with the quarter ended Dec 28, 2019.

What the Zacks Model Unveils

Our proven model does not conclusively predict a beat for Boot Barn this earnings season. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter. You can see the complete list of today’s Zacks #1 Rank stocks here.

Boot Barn has a Zacks Rank #2 but an Earnings ESP of 0.00%.

Stocks With Favorable Combination

Here are three companies you may want to consider as our model shows that these have the right combination of elements to post an earnings beat:

Crocs, Inc. CROX currently has an Earnings ESP of +32.02% and a Zacks Rank #1. The company is likely to register bottom-line improvement when it reports fourth-quarter 2021 numbers. The Zacks Consensus Estimate for quarterly earnings per share of $1.52 suggests a substantial improvement from $1.06 reported in the year-ago quarter.

Crocs’ top line is expected to rise year over year. The Zacks Consensus Estimate for quarterly revenues is pegged at $582.9 million, which indicates an improvement of 41.7% from the figure reported in the prior-year quarter. CROX has a trailing four-quarter earnings surprise of 41.6%, on average.

Macy's M currently has an Earnings ESP of +7.71% and a Zacks Rank #1. The company is likely to register bottom-line improvement when it reports fourth-quarter fiscal 2021 numbers. The Zacks Consensus Estimate for quarterly earnings per share of $1.97 suggests a substantial improvement from 80 cents reported in the year-ago quarter.

Macy's top line is expected to rise year over year. The Zacks Consensus Estimate for quarterly revenues is pegged at $8.44 billion, which indicates an improvement of 24.5% from the figure reported in the prior-year quarter. M has a trailing four-quarter earnings surprise of 313.5%, on average.

Levi Strauss & Co. LEVI currently has an Earnings ESP of +1.01% and a Zacks Rank #3. The company is likely to register an increase in the bottom line when it reports fourth-quarter fiscal 2021 numbers. The Zacks Consensus Estimate for quarterly earnings per share of 40 cents suggests an increase of 100% from the year-ago reported number.

Levi Strauss’ top line is expected to increase year over year. The Zacks Consensus Estimate for quarterly revenues is pegged at $1.68 billion, which suggests growth of 21.1% from the prior-year quarter. LEVI has a trailing four-quarter earnings surprise of 66.6%, on average.

Stay on top of upcoming earnings announcements with the Zacks Earnings Calendar.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Macy's, Inc. (M) : Free Stock Analysis Report

Boot Barn Holdings, Inc. (BOOT) : Free Stock Analysis Report

Crocs, Inc. (CROX) : Free Stock Analysis Report

Levi Strauss & Co. (LEVI) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research