Exploring Undervalued Small Caps With Insider Action In Hong Kong July 2024

Amid a backdrop of shifting market dynamics, the Hong Kong small-cap sector presents intriguing opportunities for discerning investors. With global indices reflecting a pivot towards value and small-cap shares, this article will explore three undervalued small caps in Hong Kong that are showing promising insider activity.

Top 10 Undervalued Small Caps With Insider Buying In Hong Kong

Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

China Overseas Grand Oceans Group | 2.4x | 0.1x | 11.76% | ★★★★★☆ |

Ever Sunshine Services Group | 5.6x | 0.4x | 21.41% | ★★★★★☆ |

Wasion Holdings | 10.5x | 0.8x | 37.01% | ★★★★☆☆ |

Nissin Foods | 14.2x | 1.3x | 42.04% | ★★★★☆☆ |

China Leon Inspection Holding | 9.6x | 0.7x | 29.33% | ★★★★☆☆ |

China Education Group Holdings | 7.1x | 1.7x | 49.95% | ★★★★☆☆ |

Transport International Holdings | 11.7x | 0.6x | 43.90% | ★★★★☆☆ |

Skyworth Group | 5.6x | 0.1x | -304.55% | ★★★☆☆☆ |

Kinetic Development Group | 4.0x | 1.8x | 19.31% | ★★★☆☆☆ |

Shenzhen International Holdings | 8.0x | 0.7x | 14.62% | ★★★☆☆☆ |

Let's review some notable picks from our screened stocks.

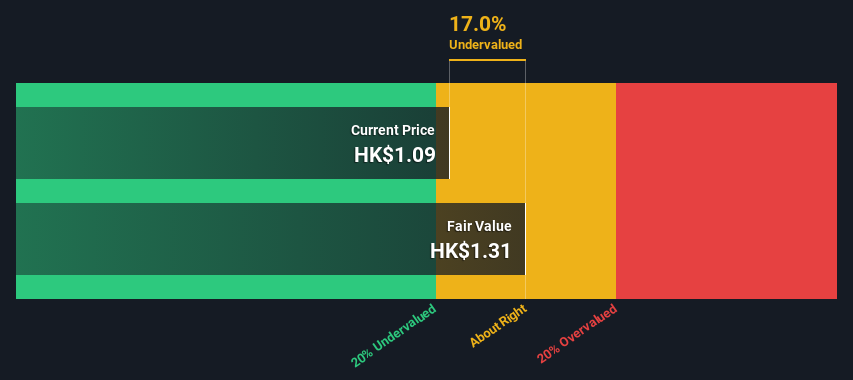

Kinetic Development Group

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Kinetic Development Group is a company involved in various business sectors with a market capitalization of approximately CN¥1.23 billion.

Operations: The company's gross profit margin has shown a notable upward trend, increasing from 9.05% in September 2013 to approximately 59.07% by July 2024. This improvement reflects a significant enhancement in the efficiency of its cost management and operational execution over the period, indicating robust growth in profitability relative to its cost of goods sold (COGS).

PE: 4.0x

Kinetic Development Group, a lesser-known entity in Hong Kong's bustling market, recently amended its corporate governance structures and reduced its annual dividend to HK$0.05 per share as of May 7, 2024. These changes reflect a strategic pivot amid a funding model reliant solely on external borrowing—considered riskier than customer deposits. Despite these challenges, insider confidence is evident from recent share purchases by executives, signaling belief in the company’s potential growth and resilience. This activity suggests that Kinetic may be poised for recovery or growth despite current financial structuring concerns.

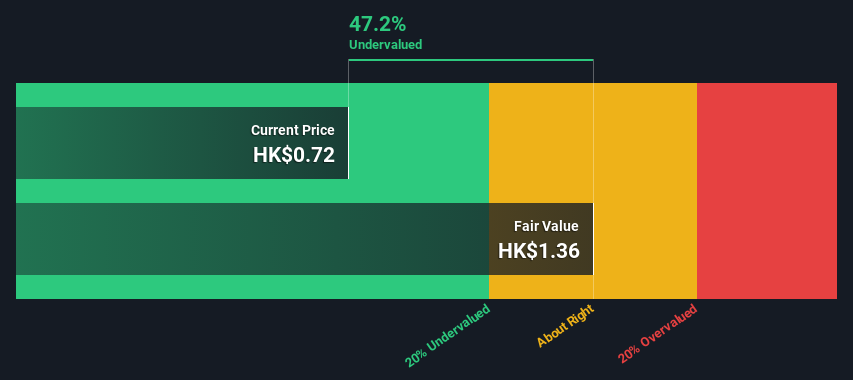

Comba Telecom Systems Holdings

Simply Wall St Value Rating: ★★★★☆☆

Overview: Comba Telecom Systems Holdings specializes in providing wireless telecommunications network system equipment and services, primarily serving operators in the telecommunications sector, with a market capitalization of approximately HK$1.53 billion.

Operations: The business generates significant revenue from wireless telecommunications network system equipment and services, amounting to HK$5.82 billion, complemented by operator telecommunication services contributing HK$157.83 million. Over recent periods, the gross profit margin has shown a trend of fluctuation with notable figures such as 28.44% in June 2016 and a decrease to 27.79% by December 2023, indicating variability in cost management relative to sales revenue.

PE: 373.2x

Comba Telecom Systems Holdings recently showcased its potential at MWC Shanghai, underscoring its market presence. Meanwhile, Tung Ling Fok's recent acquisition of 1.83 million shares signals strong insider confidence, reflecting a belief in the firm’s growth trajectory. Despite a volatile share price and lower profit margins year-over-year, the company's strategic buyback program initiated on June 3 aims to enhance shareholder value by using legally available funds. This approach could potentially bolster net assets per share and earnings.

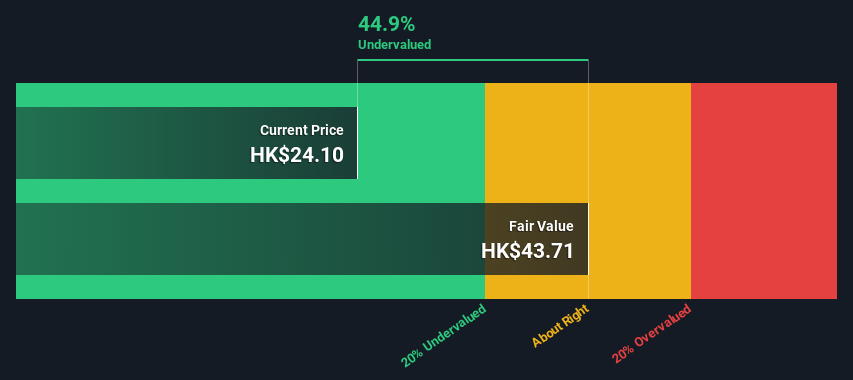

Ferretti

Simply Wall St Value Rating: ★★★★★☆

Overview: Ferretti specializes in the design, construction, and marketing of yachts and recreational boats, with a market capitalization of approximately €1.23 billion.

Operations: The business generates €1.23 billion from the design, construction, and marketing of yachts and recreational boats. It reported a net income of €83.05 million with a gross profit margin of 37.08%.

PE: 11.5x

Ferretti, a lesser-known entity in Hong Kong's market, recently showcased robust financial projections at the UniCredit Italian Investment Conference, forecasting revenue growth between 9.8% and 11.6% for 2024. Insider confidence is evident as they recently purchased shares, signaling belief in the company’s prospects despite its reliance on external borrowing—a riskier funding mechanism. With earnings expected to rise by approximately 12.46% annually, Ferretti's blend of ambitious financial targets and insider buying activity paints a promising picture for potential growth.

Click here and access our complete valuation analysis report to understand the dynamics of Ferretti.

Assess Ferretti's past performance with our detailed historical performance reports.

Next Steps

Reveal the 17 hidden gems among our Undervalued SEHK Small Caps With Insider Buying screener with a single click here.

Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Seeking Other Investments?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include SEHK:1277 SEHK:2342 and SEHK:9638.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com