Exploring Three Undiscovered Gems in Hong Kong Stocks

Amidst a backdrop of shifting market dynamics, where small-cap stocks are increasingly capturing investor interest as indicated by the Russell 2000's performance, Hong Kong's market presents unique opportunities. Exploring these lesser-known stocks could unveil potential in a landscape where discerning investors seek value and growth away from mainstream options.

Top 10 Undiscovered Gems With Strong Fundamentals In Hong Kong

Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

S.A.S. Dragon Holdings | 37.35% | 4.13% | 12.06% | ★★★★★★ |

COSCO SHIPPING International (Hong Kong) | NA | -12.97% | 12.59% | ★★★★★★ |

PW Medtech Group | NA | 17.93% | -2.70% | ★★★★★★ |

Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

Hung Hing Printing Group | 3.97% | -2.51% | 33.57% | ★★★★★☆ |

Changjiu Holdings | 14.09% | 12.87% | -4.74% | ★★★★★☆ |

Mulsanne Group Holding | 186.88% | -12.02% | -43.54% | ★★★★☆☆ |

Time Interconnect Technology | 212.50% | 27.21% | 15.01% | ★★★★☆☆ |

Laopu Gold | 8.43% | 26.56% | 36.28% | ★★★★☆☆ |

Pizu Group Holdings | 48.34% | -4.53% | -19.78% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

Xiamen Yan Palace Bird's Nest Industry

Simply Wall St Value Rating: ★★★★★★

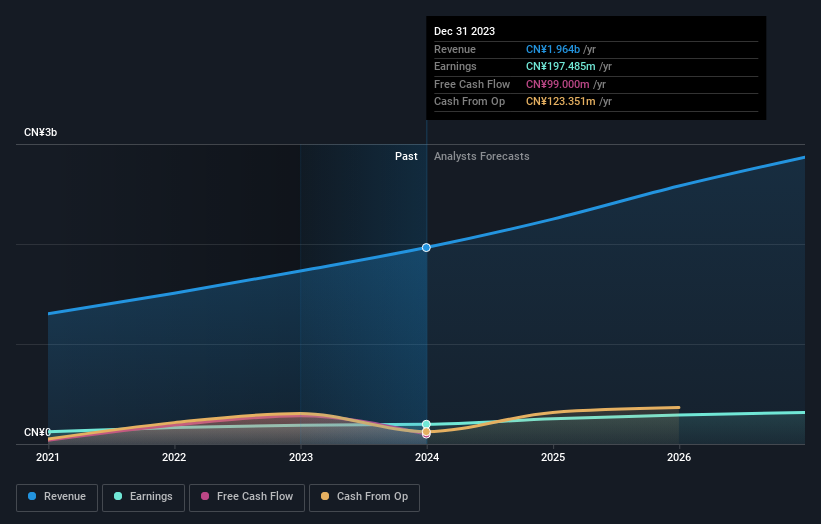

Overview: Xiamen Yan Palace Bird's Nest Industry Co., Ltd. is a company that specializes in the research, development, production, and marketing of edible bird's nest products within the People’s Republic of China, with a market capitalization of HK$6.60 billion.

Operations: The company generates revenue through diverse channels, including direct sales to online and offline customers, as well as through sales to distributors and e-commerce platforms. It has experienced growth in net income from CN¥63.29 million in 2018 to CN¥197.49 million by the end of 2023, alongside an increase in gross profit margin from 51.70% to 50.65% over the same period.

Xiamen Yan Palace Bird's Nest Industry, a lesser-known yet promising entity in Hong Kong's market, anticipates revenue between RMB 1,045 million and RMB 1,090 million for the first half of 2024—a rise of up to 15% year-over-year—despite a forecasted net profit drop of nearly 50%. This performance highlights robust online sales growth amidst tough conditions. The company remains debt-free with high-quality non-cash earnings and has outpaced its industry with a 4.9% earnings increase last year.

Plover Bay Technologies

Simply Wall St Value Rating: ★★★★★★

Overview: Plover Bay Technologies Limited is an investment holding company specializing in the design, development, and marketing of software-defined wide area network (SD-WAN) routers, with a market capitalization of HK$4.32 billion.

Operations: The company generates revenue primarily through the sale of SD-WAN wired and wireless routers, contributing $14.59 million and $49.39 million respectively, alongside software licenses and warranty and support services which add another $30.28 million. It has shown a notable trend in net income margin improvement, reaching 29.81% by the end of 2023 from earlier figures around 19%.

Plover Bay Technologies, a lesser-known entity in the Hong Kong market, has recently demonstrated robust financial and operational performance. With a 24% earnings growth surpassing the Communications industry's 10.6%, and a forecast for future earnings growth at 16.59% annually, the company shows promising potential. Its debt to equity ratio improved significantly from 4% to 2.3% over five years, reflecting stronger balance sheet management. Moreover, trading at 57% below its estimated fair value suggests an attractive investment opportunity. Recent dividends and substantial net profit increases further underscore its upward trajectory in both sales volume and profit margins.

Dive into the specifics of Plover Bay Technologies here with our thorough health report.

Understand Plover Bay Technologies' track record by examining our Past report.

MicroPort NeuroTech

Simply Wall St Value Rating: ★★★★★★

Overview: MicroPort NeuroTech Limited specializes in the R&D, manufacturing, and sale of neuro-interventional medical devices, serving markets in the People’s Republic of China and globally, with a market capitalization of HK$4.54 billion.

Operations: This entity primarily generates revenue through its surgical and medical equipment segment, evidenced by consistent sales figures such as CN¥665.62 million reported in the most recent period. The company's cost of goods sold (COGS) was CN¥153.83 million, with gross profit reaching CN¥511.79 million during the same timeframe, indicating a significant value-add through its manufacturing and distribution processes.

MicroPort NeuroTech, recently rebranded as MicroPort NeuroScientific Corporation, is capturing attention with its robust performance in the medical equipment sector. Despite a challenging industry backdrop with an average earnings decline of 8.3%, the company has pivoted to profitability this year and is outpacing peers with a forecasted annual earnings growth of 31.7%. Impressively, it operates debt-free and reported a significant revenue surge to RMB 400-410 million for the first half of 2024, up by about 35% year-over-year. This financial vitality is complemented by strategic leadership changes and corporate governance enhancements, positioning it as a compelling entity in its niche market.

Where To Now?

Investigate our full lineup of 178 SEHK Undiscovered Gems With Strong Fundamentals right here.

Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Want To Explore Some Alternatives?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include SEHK:1497 SEHK:1523 and SEHK:2172.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com