Yahoo Finance

Yahoo Finance DBS cuts overall DPU estimates and target prices for S-REITs on slower growth momentum

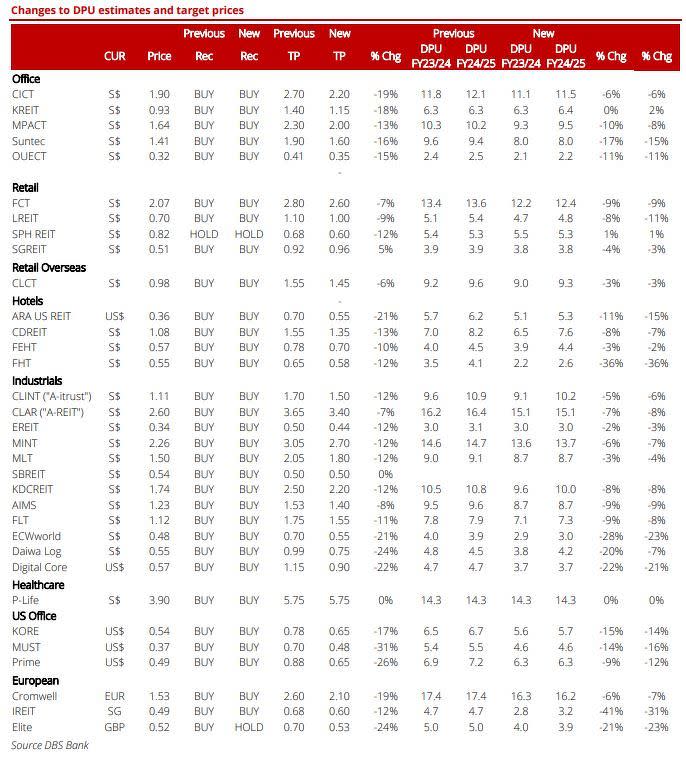

The DBS analysts have lowered their DPU estimates on the S-REIT sector by 7% and TPs by 11% based on their revised estimates.

DBS Group Research analysts Derek Tan, Rachel Tan, Dale Lai and Geraldine Wong have cut their distribution per unit (DPU) estimates and their target prices for the overall Singapore REIT (S-REIT) sector following the recent results season.

Even though the sector enjoyed a general near-term rebound in prices as the consumer price index (CPI) print for October in the US was cooler than expected, the analysts saw the results season as “an opportunity” for them to revisit their estimates given the higher-than-expected rise in base rates at 200 basis points from 100 basis points before.

The analysts have also updated their currency assumptions to spot rates, which have resulted in changes to their estimates for foreign-focused S-REITs.

“Overall, the revised estimates have resulted in a 7% cut in our FY2023/FY2024 DPU and a reduction of [around] 11% in our target prices, as we factor higher discount rates into our valuation models,” the analysts write in their Nov 18 report.

“Based on our revised estimates, the S-REITs are now forecast to deliver a FY2022-FY2024 DPU growth of 2.0% (or -0.2% ex-hospitality) with the hospitality S-REITs still projected to deliver a two-year compound annual growth rate (CAGR) of 16.0%, while the rest of the subsectors range between -1% to +2.0% growth, led by office and China-focused S-REITs,” they add.

According to the analysts’ revised estimates, S-REITs are now trading at an FY2023 yield of 6.1%, which implies a yield spread of 2.9% against the 10-year bond yield. The 10-year bond yield has retreated to 3.25% after peaking at 3.5% in the week starting Nov 7.

Investors should focus on the economic outlook and resiliency of S-REITs’ earnings trajectory

Looking ahead, investors should move on from the US Federal Reserve (US Fed) rate hikes to the economic outlook and risk of a recession.

In their report, the analysts note that DBS’s economists believe that “inflation fear” has peaked. A thawing of relations between the US and China, as well as the expected gradual re-opening of China “sometime in 2023” may further cool inflationary pressures in 2023.

The US Fed is also expected to taper off its 75-basis point hikes at the Federal Open Market Committee (FOMC) meetings beginning in December.

On Nov 24, it was reported that US Fed officials were leaning towards moderating their pace of rate hikes to mitigate risks of overtightening. There were also signs that they were leaning towards a 50 basis-point hike in December instead of their previous 75-basis point hikes.

“In our recent conversations, we have highlighted to investors that with the rate hikes peaking and inflation fear behind us, we believe that conversations will gradually switch focus from the Fed hikes to the economic outlook and resiliency of S-REITs’ earnings trajectory, given concerns about an overall slowdown,” the analysts write.

Among the S-REIT subsectors, they have, however, kept their picks unchanged.

Preferring more resilient names, Frasers Centrepoint Trust (FCT) and Lendlease Global Commercial REIT (LREIT) are still the analysts’ picks among the suburban retail REITs while Mapletree Logistics Trust (MLT) and Mapletree Industrial Trust (MINT) are their picks among the industrial S-REITs.

“Best-in-class” names such as Keppel REIT and Mapletree Pan Asia Commercial Trust (MPACT) have also been selected as the analysts’ top picks among commercial S-REITs.

CDL Hospitality Trust (CDLHT) has also been identified as the analysts’ top pick among the hospitality names even as the sector has lost some momentum recently. “[The sector] could still see another round of rallying upon China re-opening for travel, which we believe will be the [sector’s] next leg of re-rating.”

For the full set of changes, please refer to the table below.

See Also:

Click here to stay updated with the Latest Business & Investment News in Singapore

CGS-CIMB ups Boustead Projects' TP on strong order book and stronger-than-expected 1HFY2023 earnings

Analysts mixed on ComfortDelGro's outlook after 3QFY2022 earnings miss

DBS maintains 'buy' on Digital Core REIT on further DPU accretion

Get in-depth insights from our expert contributors, and dive into financial and economic trends