Yahoo Finance

Yahoo Finance

DBS: Asian Equities Outlook For 2Q17

The stock market has always been driven by emotions rather than logic. In 1Q2017, the single and most unlikely source drove stock markets into new heights: Mr Donald J. Trump.

President Trump’s anti-globalisation and trade war threats were shrouded by his ‘American First’ promise and his push to unwind the Dodd-Frank act. The market has since returned to its rational state and has taken a step back as President Trump faces obstacles in wielding his powers. So how should investors look at the market in the next few months?

Stronger global growth but political risks aplenty

Economists at DBS are certain that growth will continue to pick up its pace. Yet, the headwinds from political risks could potentially derail global growth back to post-GFC levels. Political risks include trade conflicts between US and China, break up of Eurozone (if Marine Le Pen gets elected) and nuclear threats from North Korea.

Looking ahead, there are four investment themes that DBS Research believes will drive investments in Asia in the next few months.

4 Investment Themes For Asia

1. Global Cyclical Expansion Goes Ahead, With Or Without US

from Trey Ratcliff at www.stuckincustoms.com

DBS believes that US’s threats of a trade war with China will not materialise. Even if it does, it will not be what the world fears. This is because, in DBS’s view, China and Asia are the regions in the world that are still growing. Should the US decide to initiate a meaningless trade war with China, US will be the only loser from its own actions.

China – and the rest of Asia – will not be impacted and will continue to ride on its cyclical expansion. Moreover, there is strong evidence of growing demand for electronic components such as Wifi, IT infrastructure and electronic gadgets to support digitalisation in Asia.

2. Fiscal policies will stimulate growth

After years of leveraging on monetary policies to stimulate economies, world leaders are now turning their focus towards fiscal expansion, i.e. reflation. This comes after years of fiscal contraction. Fiscal expansions will lead to higher demand for commodity prices as countries expand their infrastructure investments. This will help economies achieve healthy levels of inflation to re-ignite global economic growth, which should trickle down to Asian economies.

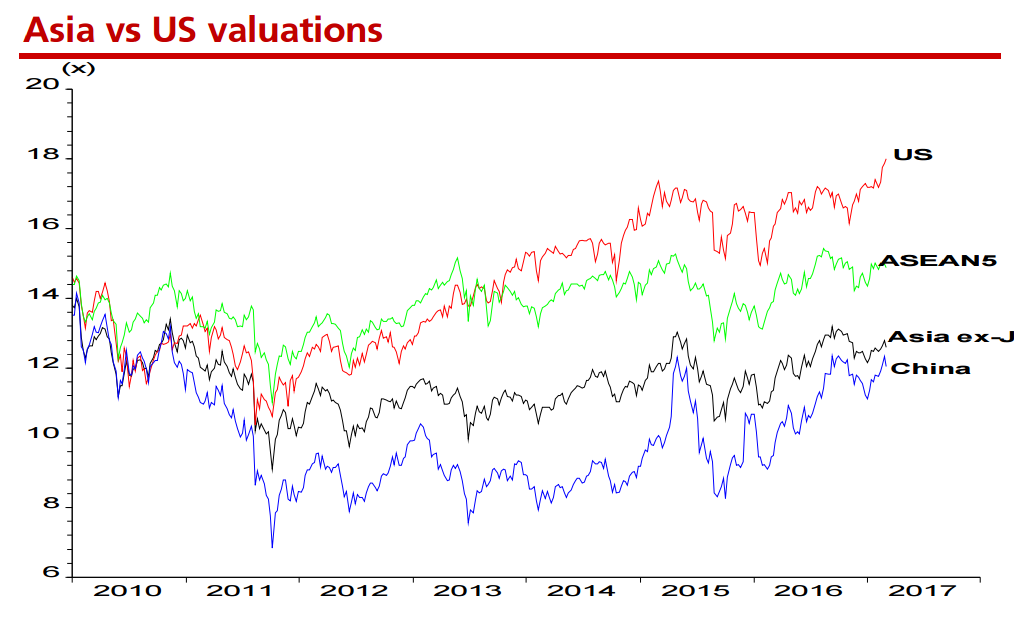

3. Asian valuations in tandem with the US valuations

Source: CIMB

Asian markets have always been “followers” of the US market. Unsurprisingly, Asian markets have performed in tandem with the euphoric performance in the US markets in 1Q17. For example, the banking sector had a good performance in 1Q17 as it benefitted from rising interest rates in the US and easing restrictions of the Dodd-Frank regulations. DBS opines that further deregulations and policies from Trump’s administration will lead to corresponding outperformance in Asia.

4. ASEAN Domestic Demand

Apart from the US and China, DBS believes that there are two key drivers that will drive Asia’s growth: domestic government investments and private consumption. Market consensus has given these two sectors higher earnings growth forecasts than the overall domestic market, which reflects the market’s confidence in these sectors to lead growth in ASEAN.

Investors Takeaway: Focus On Singapore & HK Markets

Among the Asian markets, DBS recommends investors to focus on Singapore and Hong Kong. These two markets have outperformed the US market in Q1 due to its stable policies and premium growth prospects. DBS is confident that Singapore’s cheap valuations and cyclical rebound will enhance Singapore as a defensive option for the portfolio.

The Hong Kong market will reap benefits from earnings growth recovery in the stabilising Chinese economy. With H-shares still trading at a discount to A-shares, positive sentiments towards the Chinese economy can help to turn those discounts into capital gains for investors.

Stay tuned for the next article on DBS’s Singapore and Hong Kong Equities Outlook!

Featured Upcoming Event

Learn how you can profit in the “New World Order” at our half-yearly Shares Investment Conference (SIC1H2017) from Dr Chan Yan Chong and other experts. To find out more about the event, please click on the button below. (This is a Chinese event)

Remember to enter the discount code "SIC10" for a $10-discount off your ticket price!