Crude Oil Primed for Explosive Short-Squeeze as Bearish Sentiment Peaks

US oil production continues to show signs of stagnant growth

With sentiment and positioning at all-time bearish levels, oil prices are poised for a significant short-squeeze to the upside.

Should US oil production growth continue to disappoint, the energy bull market is likely to continue.

Central to my bullish long-term thesis for energy is the slowing growth in US oil and natural gas production. I recently delved into this dynamic in depth here, detailing how we are seeing signs of a forthcoming peak in US oil production.

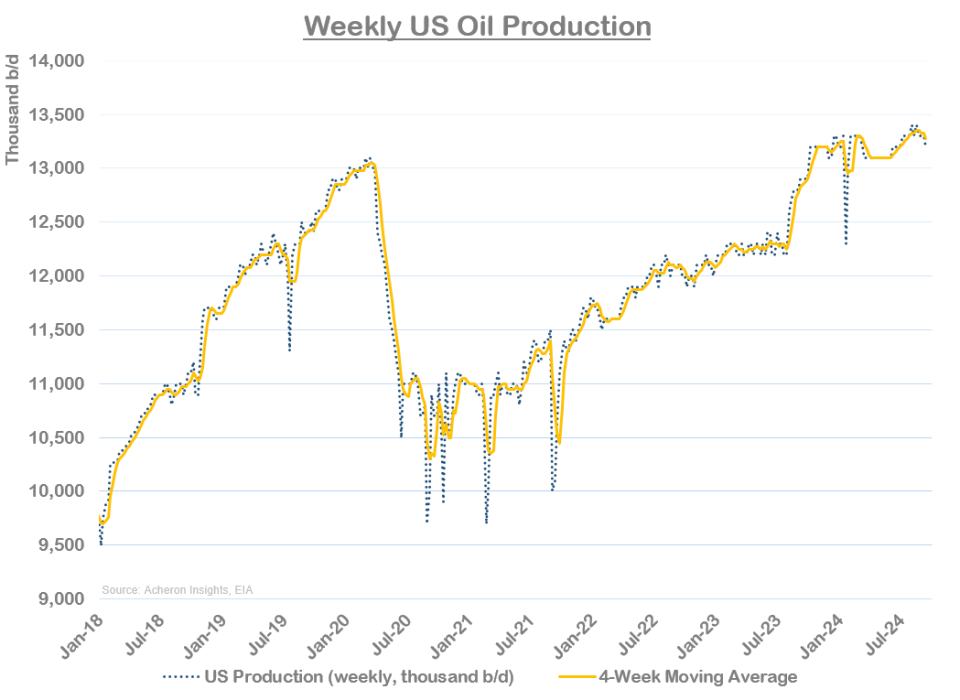

Through September, we continue to see evidence of lackluster oil production. As we can see below, the EIA’s weekly implied production data has been flat for 12 months now.

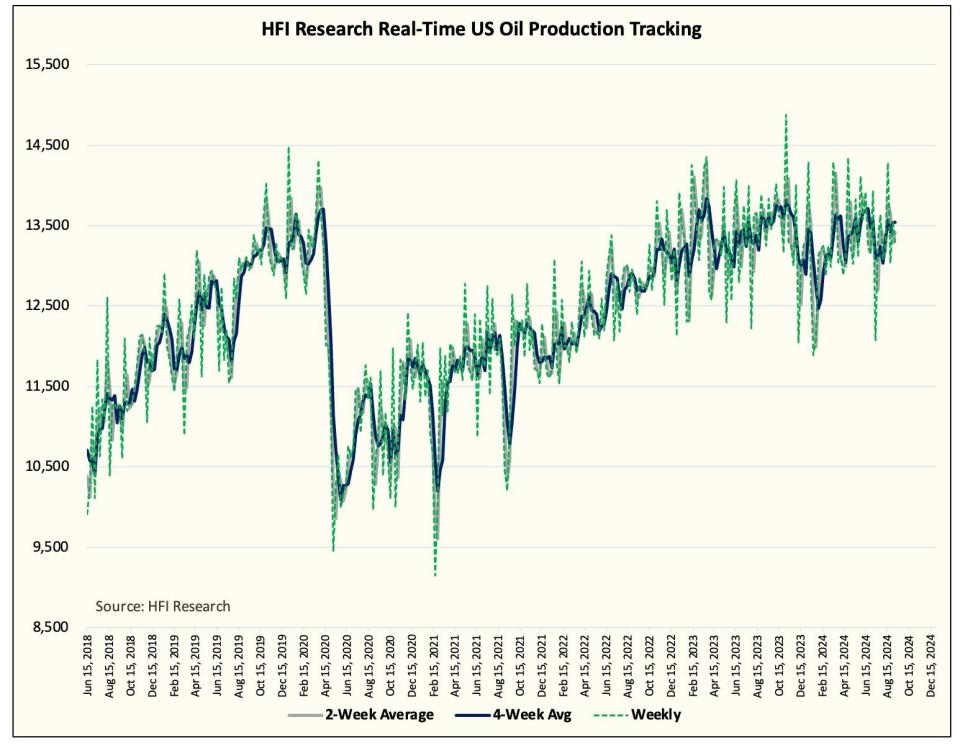

Although the EIA’s weekly production numbers are unreliable, given they are merely estimates (compared to the much more reliable monthly data), this is another signpost supporting the idea US oil production growth is challenged. Importantly, other real-time measures of US oil production are confirming this dynamic, as we can see below courtesy of HFI Research.

As I detailed in my previous article, US oil production growth is likely to surprise to the downside in 2024. This is seemingly playing out thus far.

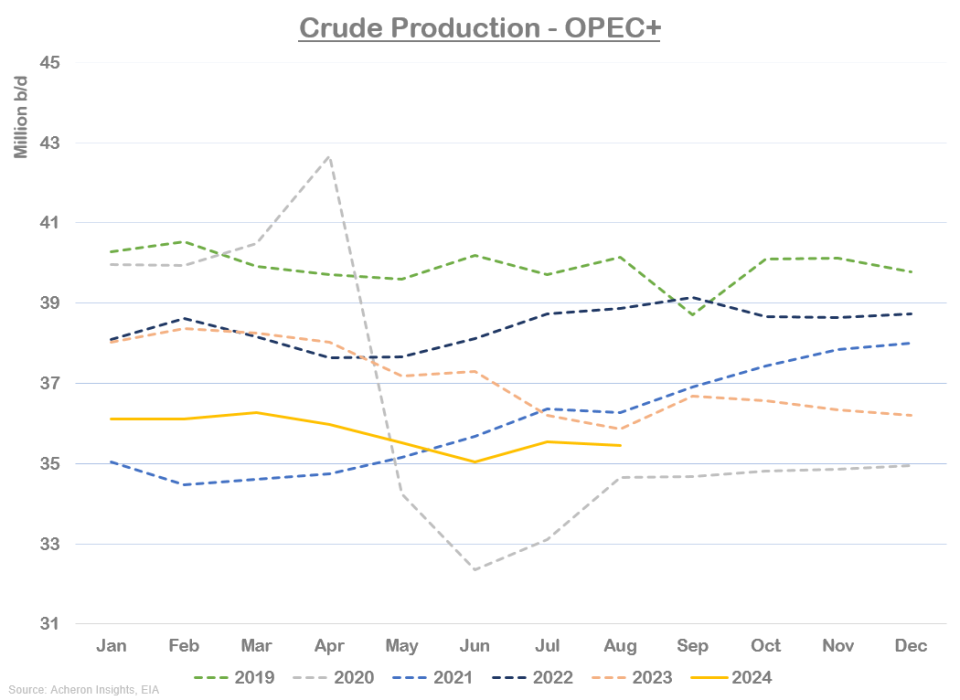

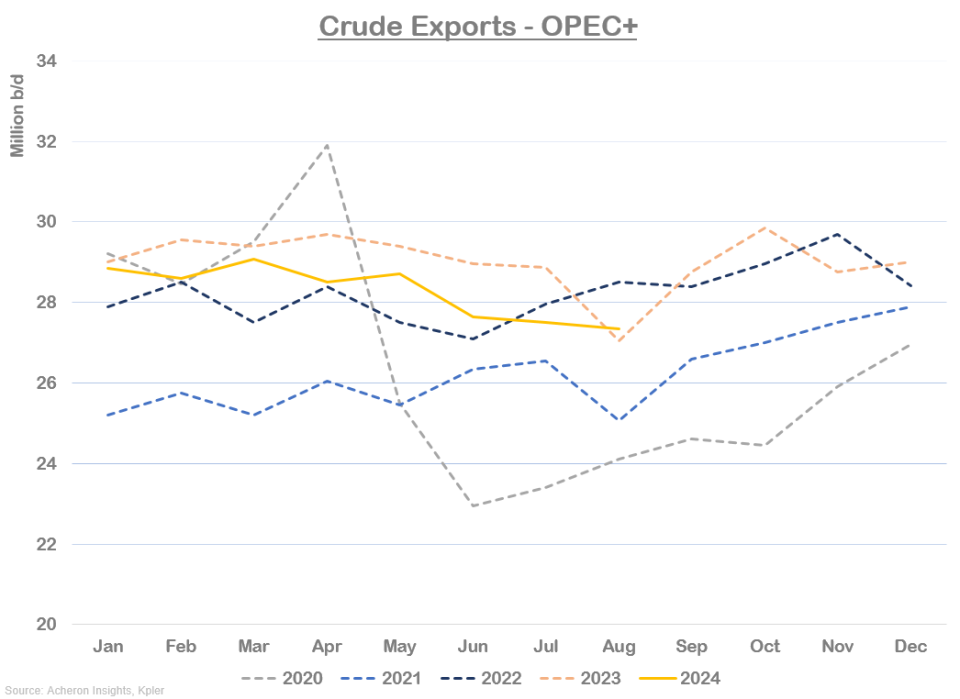

In addition to US supplies, OPEC+ production cuts are only just now translating into falling exports. As we can observe below, despite OPEC+ production being at its lowest levels since 2020, it was only up until the past few months actual OPEC+ exports have started to decline.

For the first six months of 2024, exports were well above 2022 and 2021 levels.

The point here is the actual supply reductions from OPEC+ production cuts have up until recently been much smaller than consensus would have you believe, meaning the unwinding of forthcoming production cuts come December is unlikely to be as bearish as the market expects.

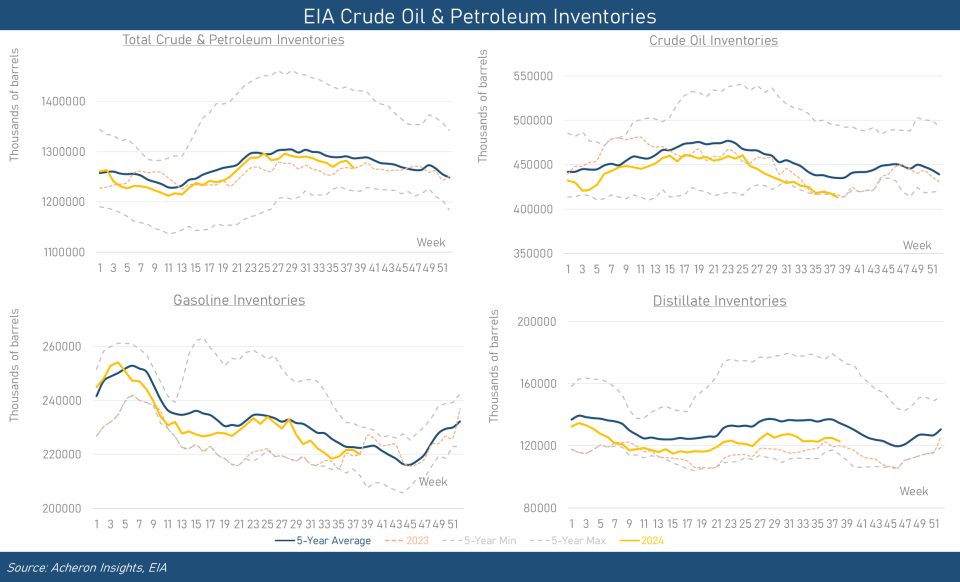

Inventories Have Been Drawing Down

What we have also seen over recent months is relatively bullish changes in inventories. Although draws have been inconsistent relative to seasonal averages, crude oil inventories in particular have drawn down quite significantly over the past three months. Even though total crude and petroleum inventories have not drawn to the same extent, US crude inventories now stand at five-year lows.

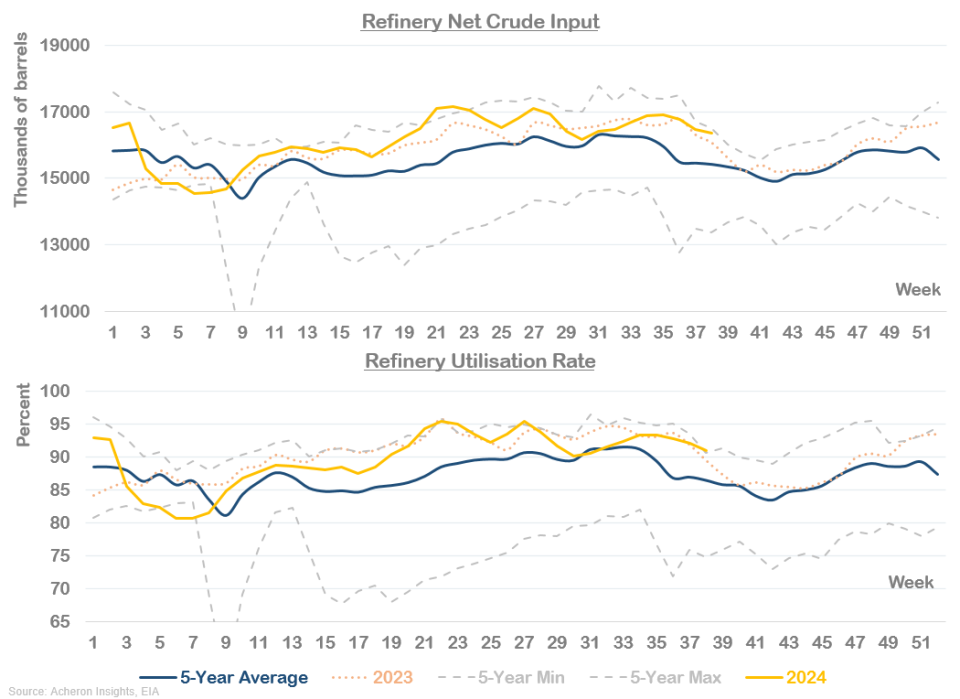

What has been driving crude draws relative to other petroleum products has been persistently above-average refinery runs, as we can see below.

So Why Are Oil Prices Falling?

If crude inventories are seeing persistent draws, US oil production has been flat for 12 months and OPEC+ exports have now started to actually fall, why have oil prices been so weak?

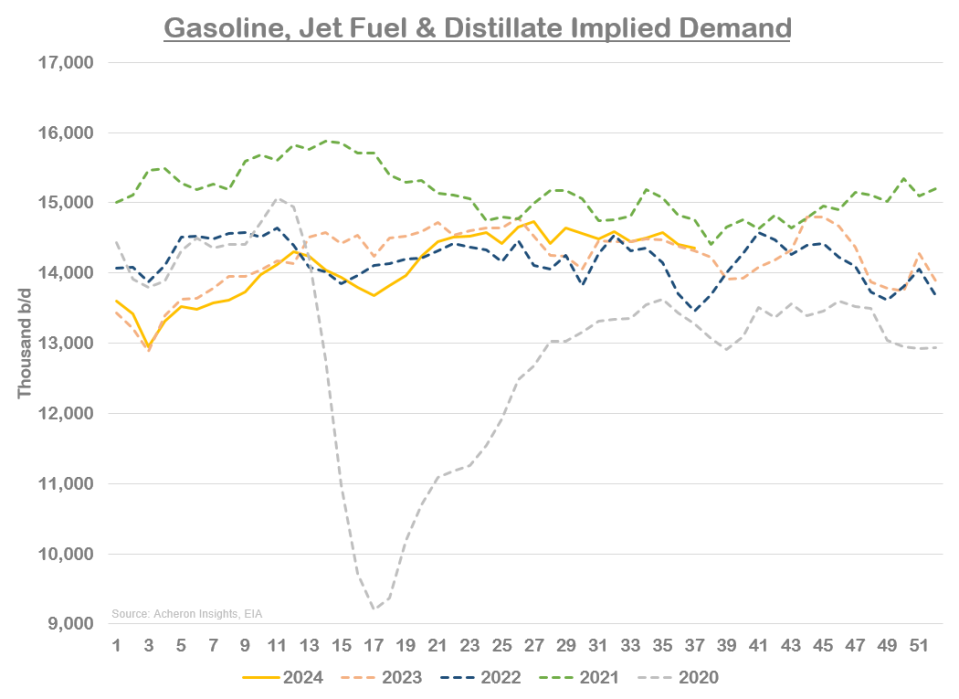

The answer to that is fairly simple. It has been a demand story. We simply haven’t seen sufficient refined product demand globally to push down total inventories and incentivize traders to bid prices higher. They have been doing the exact opposite in fact, as we shall see shortly.

Though not awful, US demand for gasoline, jet fuel, and diesel has been mediocre over the past year.

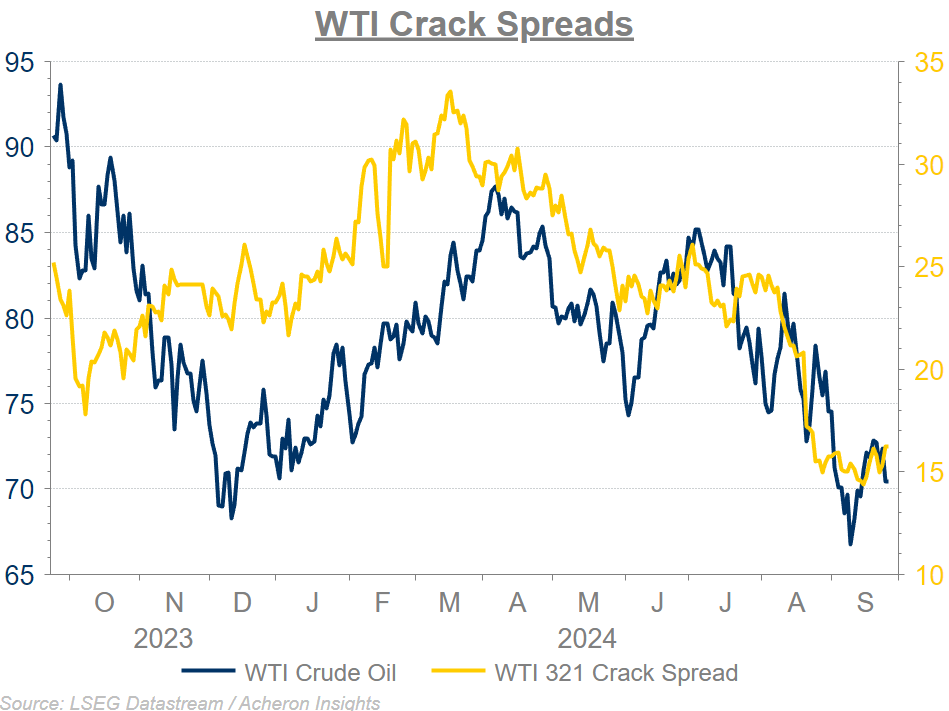

This mediocre demand has driven crack spreads significantly lower. We should start to see this begin to translate into refinery run cuts, which in turn should help tighten refined product markets and push margins higher.

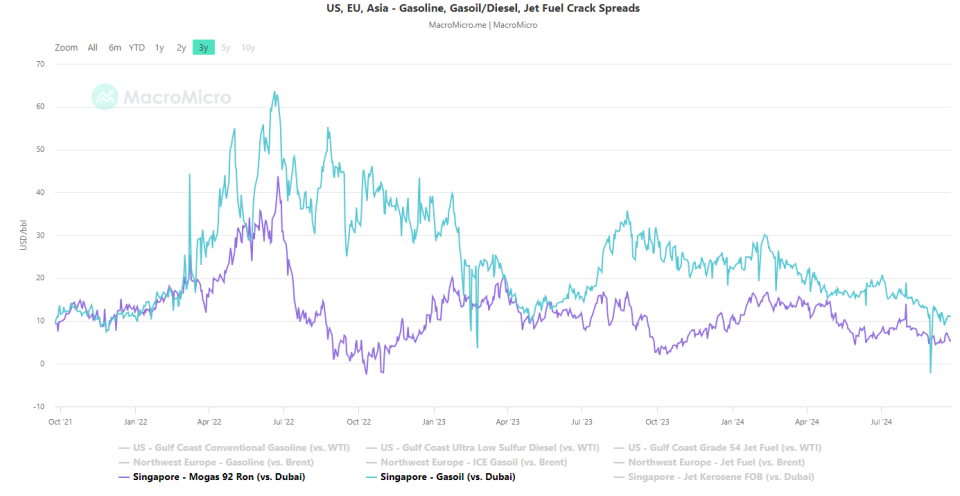

But far more important than US demand has been global oil demand, particularly in China. As we can see below, Singapore gasoil and gasoline crack spreads (an excellent proxy for Chinese demand) have been in freefall over the past year. Both now sit at four-year lows.

We all know the struggles China’s economy is dealing with at present, and we can see below how this has translated into flat crude oil imports in recent years.

Estimates of the decline in Chinese oil demand are around 1.7mm b/d over the past year. While some of this can be attributed to the rise in LNG vehicle sales in addition to China’s low-cost production of EVs, the majority of this decline in oil demand relates to economic weakness.

Positioning and Outlook

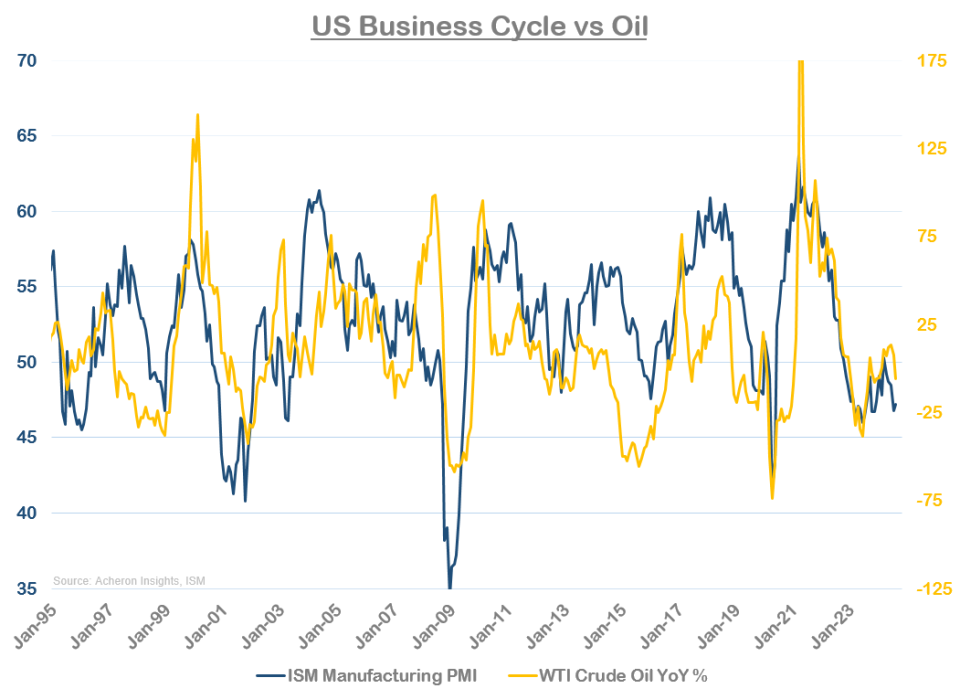

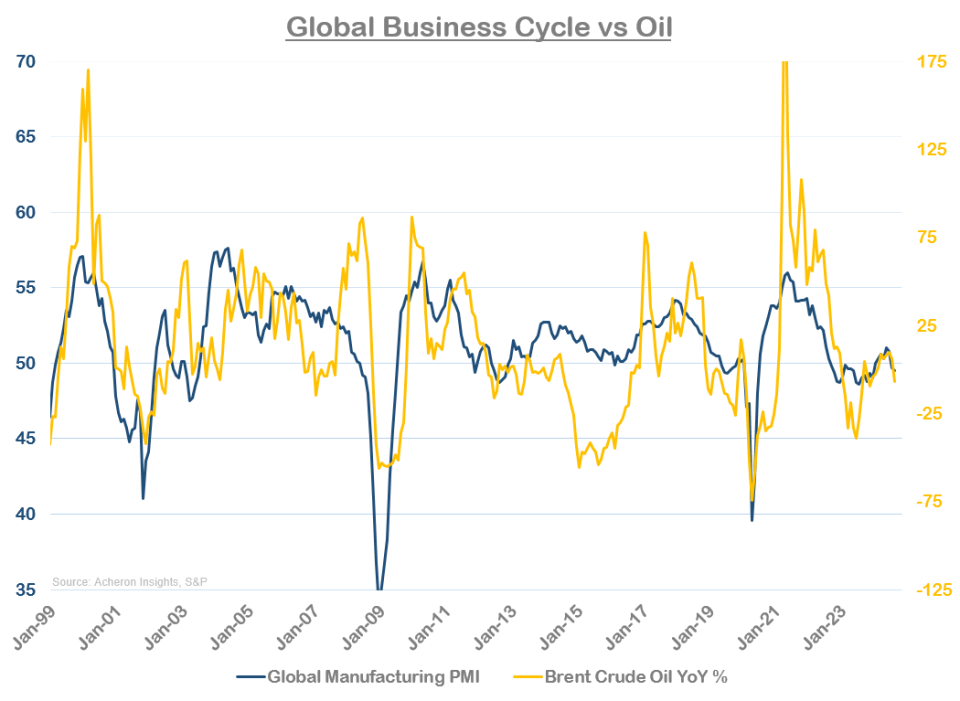

Once US, Chinese and global economic growth begins to trend higher, oil prices will follow suit. I detailed briefly here my latest thoughts on the outlook for US and global growth, but the essence is we should continue to see robust US and European economic activity that should begin to surprise to the upside.

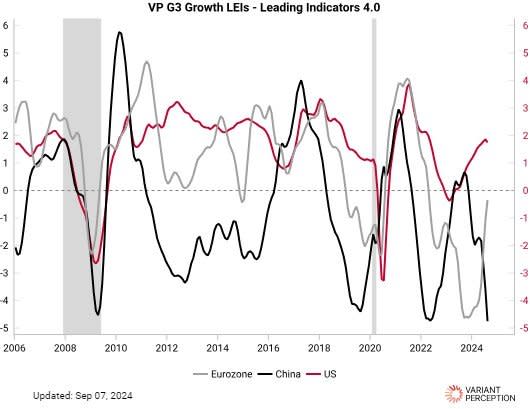

The big issue of course is the outlook for the Chinese economy. Despite their latest stimulus package, Chinese economic lead indicators remain poor, as we can see below courtesy of macro research firm Variant Perception.

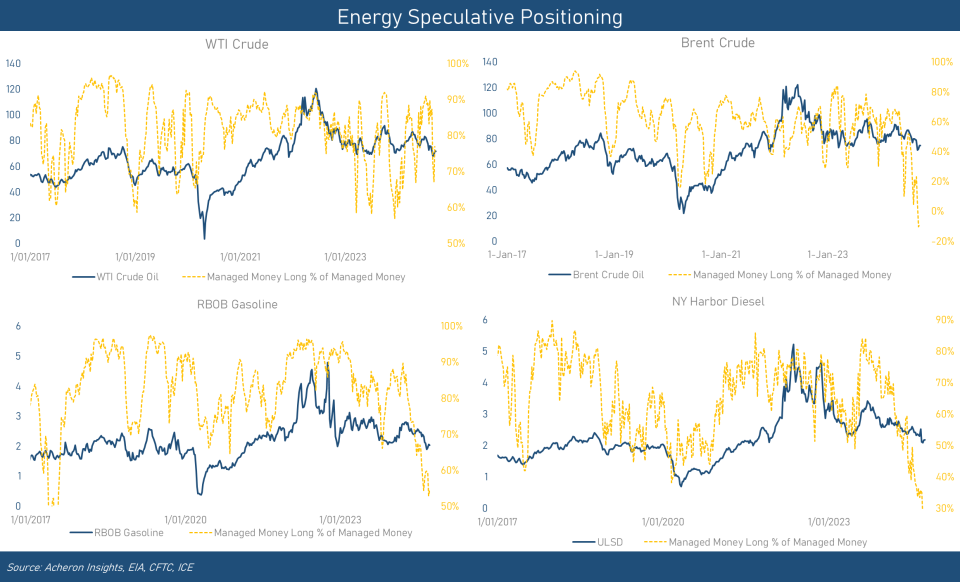

While the growth story may remain a headwind in the short to medium term, one dynamic likely to boost oil prices in the immediate future is sentiment and positioning. Simply put, sentiment toward oil has rarely been as bearish as it has been in recent weeks. This is being reflected in speculative positioning of the oil complex, as we can see below. Although WTI positioning is perhaps slightly more neutral, Brent and Diesel positioning has never been this bearish, while Gasoline positioning is at five-year lows.

This will inevitably result in a mother of all short-squeezes and puts asymmetry firmly to the upside for energy prices, particularly if economic data starts to surprise to the upside.

But for now, how higher prices rise in the short term will ultimately depend on a number of factors. Keep an eye on crack spreads and total crude and petroleum inventory draws, as the trend in both will determine the severity of the impending short-squeeze.

If cracks do not hold up and growth remains anemic, expect prices to hover around $70-$80 over the medium term. beyond that, once growth returns, and should the supply side continue to falter in the US, the long-term bull case for energy remains as positive as ever. Energy bulls should use such sell-offs as an opportunity to add to long-term holdings in the energy space, with my preferred energy exposure being the offshore services and drillers, who remain cheap as chips and should benefit handsomely from slowing shale production growth.

Related Articles

Crude Oil Primed for Explosive Short-Squeeze as Bearish Sentiment Peaks

Crude Slides Below 20 SMA, Testing Critical Support Levels Amid Bearish Signals

Gold Rises to 16% of Global Reserves: A Warning Sign for the US Dollar?