Yahoo Finance

Yahoo Finance Comerica (CMA) Q4 Earnings Beat Estimates, Revenues Fall

Comerica CMA delivered a fourth-quarter 2021 positive earnings surprise of 3.11%. Earnings per share of $1.66 surpassed the Zacks Consensus Estimate of $1.61. However, bottom line came in lower than the prior-year quarter figure of $3.43.

CMA’s results were supported by lower provisions and a robust fee income. Nevertheless, lower revenues due to reduction in net interest income (NII) were recorded. Moreover, higher expenses and a decline in loan balance were major drags.

Net income came in at $221 million in the quarter, up 2.8% year over year from $215 million.

In 2021, net income totaled $1.14 billion or $8.35 per share, up from the prior year’s $482 million or $3.43 per share. Full-year earnings outpaced the Zacks Consensus Estimate of $8.28.

Segment-wise, on a year-over-year basis, net income decreased 7% at Commercial Bank. Wealth Management and Retail segments reported a substantial year-over-year jump in net income. The Finance segment reported a loss, down 14% from the year-ago reported loss.

Revenues Fall on Lower NII, Expenses Increase

Comerica’s fourth-quarter net revenues were $750 million, down 74% year over year. Nonetheless, the top line beat the consensus estimate of $735.4 million.

NII decreased 1.7% on a year-over-year basis to $461 million in the quarter on lower rates. The NIM contracted 32 basis points to 2.04%.

Total non-interest income was $289 million, up 9.1% on a year-over-year basis. Higher fiduciary income, service charges on deposit accounts, commercial lending fees, derivative income and other noninterest income mainly supported the fee income.

Non-interest expenses totaled $486 million, up 4.5% year over year. The upswing resulted chiefly from higher salaries and benefit expenses, outside processing fees and occupancy expenses.

The efficiency ratio was 64.61% compared with the prior-year quarter’s 63.26%. A rise in the ratio indicates lower profitability.

Decent Balance-Sheet Position

As of Dec 31, 2021, total assets and common shareholders' equity were $96.69 billion and $7.8 billion, respectively, compared with $85.3 billion and $7.9 billion each as of Dec 31, 2020.

Total loans declined marginally on a sequential basis to $47.83 billion.

Nonetheless, total deposits increased 6.9% from the prior quarter’s level to $84.5 billion.

Strong Credit Quality

Total non-performing assets decreased 25.1% year over year to $269 million. The allowance for credit losses was $618 million, down from $992 million in the prior-year quarter. The allowance for loan losses to total loans ratio was 1.26% as of Dec 31, 2021, down from 1.9% as of Dec 31, 2020.

Net credit-related recoveries were $4 million compared with net credit-related charge-offs of $29 million in the prior-year quarter. A benefit to provision for credit losses of $25 million was recorded in the reported quarter compared with $17 million in the prior-year quarter.

Weak Capital Position

As of Dec 31, 2021, CMA's tangible common equity ratio was 7.30%, down from 8.02% in the prior-year quarter. The total capital ratio was 12.37%, declining from 13.20% in the year-ago quarter.

Common Equity Tier 1 (CET1) capital ratio was 10.15%, falling from 10.34% in the prior-year quarter.

Solid Capital-Deployment Activities

In the reported quarter, Comerica returned $139 million to its shareholders through share repurchases and dividends. CMA repurchased $50 million of common stock under its share repurchase program and declared dividends of $89 million on its common stock.

Our Viewpoint

Comerica's prospects look promising as strategic initiatives are likely to boost its performance. Also, lower provisions and a strong credit quality acted as tailwinds. Nevertheless, a restricted top-line expansion, eroded by a lower margin and NII, and an elevated expense base are concerns.

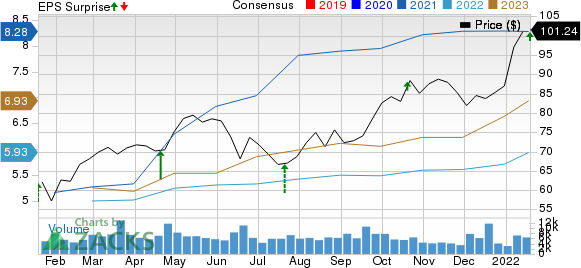

Comerica Incorporated Price, Consensus and EPS Surprise

Comerica Incorporated price-consensus-eps-surprise-chart | Comerica Incorporated Quote

Currently, Comerica carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Performance of Other Banks

Bank of New York Mellon Corporation’s BK fourth-quarter 2021 adjusted earnings of $1.04 per share surpassed the Zacks Consensus Estimate of $1.02. The bottom line improves 8.3% from the prior-year quarter’s level.

For 2021, BK’s earnings per share (GAAP basis) of $4.14 increased 8% from the 2020 figure. The Zacks Consensus Estimate for earnings was $4.17 per share. Net income applicable to common shareholders was $3.55 billion, up 4% year over year.

First Republic Bank’s FRC fourth-quarter 2021 earnings per share of $2.02 surpassed the Zacks Consensus Estimate of $1.91. Additionally, the bottom line improved 26.3% from the year-ago quarter’s level.

FRC’s quarterly results were supported by an increase in net interest income and non-interest income. Moreover, First Republic’s balance-sheet position was strong in the quarter. However, higher expenses and elevated net loan charge-offs were the offsetting factors.

Citigroup C delivered an earnings surprise of 5.04% in fourth-quarter 2021. Income from continuing operations per share of $1.46 outpaced the Zacks Consensus Estimate of $1.39. However, the reported figure declined 24% from the prior-year quarter’s tally.

Citigroup’s investment banking revenues jumped in the quarter under review, driven by equity underwriting as well as growth in advisory revenues. However, fixed-income revenues were down due to declining rates and spread products.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Citigroup Inc. (C) : Free Stock Analysis Report

The Bank of New York Mellon Corporation (BK) : Free Stock Analysis Report

Comerica Incorporated (CMA) : Free Stock Analysis Report

First Republic Bank (FRC) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research