ASX Growth Companies With At Least 10% Insider Ownership

Amidst fluctuations in commodity prices and a slight anticipated dip in the ASX200, investors continue to navigate the complexities of the Australian market. In such an environment, growth companies with high insider ownership can offer a unique appeal, potentially aligning management interests closely with shareholder outcomes in these turbulent times.

Top 10 Growth Companies With High Insider Ownership In Australia

Name | Insider Ownership | Earnings Growth |

Hartshead Resources (ASX:HHR) | 13.9% | 86.3% |

Cettire (ASX:CTT) | 28.7% | 29.9% |

Gratifii (ASX:GTI) | 15.6% | 112.4% |

Acrux (ASX:ACR) | 14.6% | 115.3% |

Alpha HPA (ASX:A4N) | 26.3% | 95.9% |

Botanix Pharmaceuticals (ASX:BOT) | 11.4% | 120.9% |

Hillgrove Resources (ASX:HGO) | 10.4% | 45.4% |

Change Financial (ASX:CCA) | 26.6% | 85.4% |

Plenti Group (ASX:PLT) | 12.8% | 106.4% |

Liontown Resources (ASX:LTR) | 16.4% | 63.9% |

We're going to check out a few of the best picks from our screener tool.

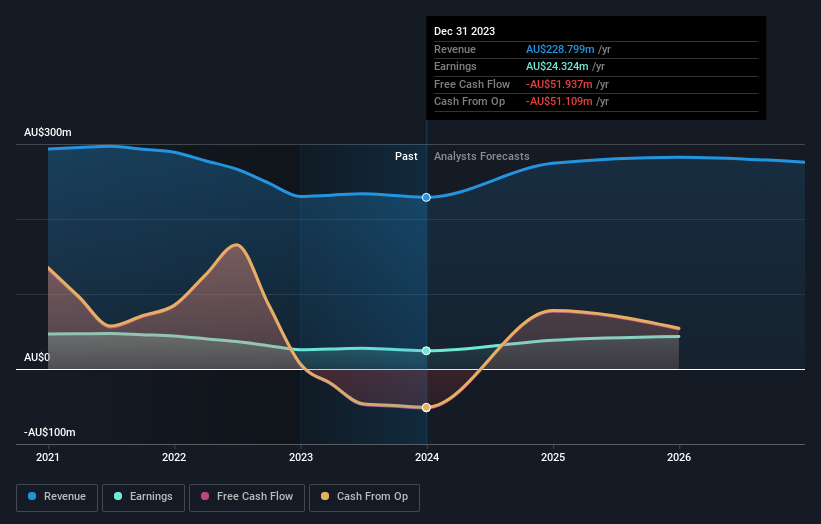

Bell Financial Group

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Bell Financial Group Limited, operating in Australia, offers a range of services including broking, online broking, corporate finance, and financial advisory to private, institutional, and corporate clients with a market capitalization of approximately A$0.42 billion.

Operations: The company generates revenue through four primary segments: retail broking (A$103.58 million), institutional broking (A$50.36 million), financial products and services (A$48.10 million), and technology and platform services (A$26.20 million).

Insider Ownership: 10.7%

Bell Financial Group is poised for notable growth, with earnings expected to increase by 26.95% annually over the next three years, outpacing the Australian market's forecast of 13.9%. Despite a low return on equity forecast at 16.3%, the company trades at a significant discount of 25.3% below estimated fair value, suggesting potential undervaluation. Revenue growth projections stand at 5.6% per year, slightly above the market average of 5.3%. However, its dividend sustainability is questionable as it is not well covered by earnings or cash flows.

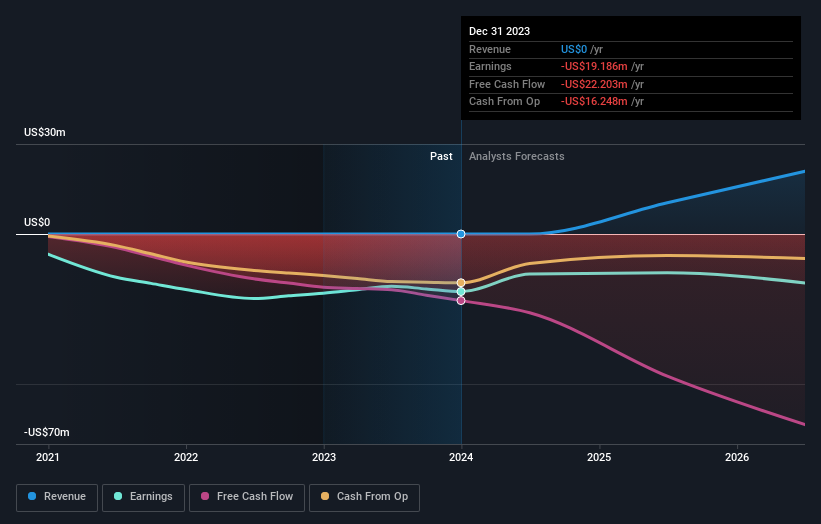

Botanix Pharmaceuticals

Simply Wall St Growth Rating: ★★★★★★

Overview: Botanix Pharmaceuticals Limited, based in Australia, focuses on the research and development of dermatology and antimicrobial products with a market capitalization of approximately A$448.91 million.

Operations: The company generates revenue primarily from its research and development activities in dermatology and antimicrobial products, totaling A$0.44 million.

Insider Ownership: 11.4%

Botanix Pharmaceuticals, with less than A$1 million in annual revenue, is on a trajectory for substantial growth. Its earnings are forecast to increase by 120.89% annually over the next three years, significantly outpacing the Australian market. However, shareholder dilution occurred over the past year and it has less than one year of cash runway. Recently added to the S&P/ASX All Ordinaries Index, Botanix is preparing for commercial launch as it nears planned approval of SofdraÔ.

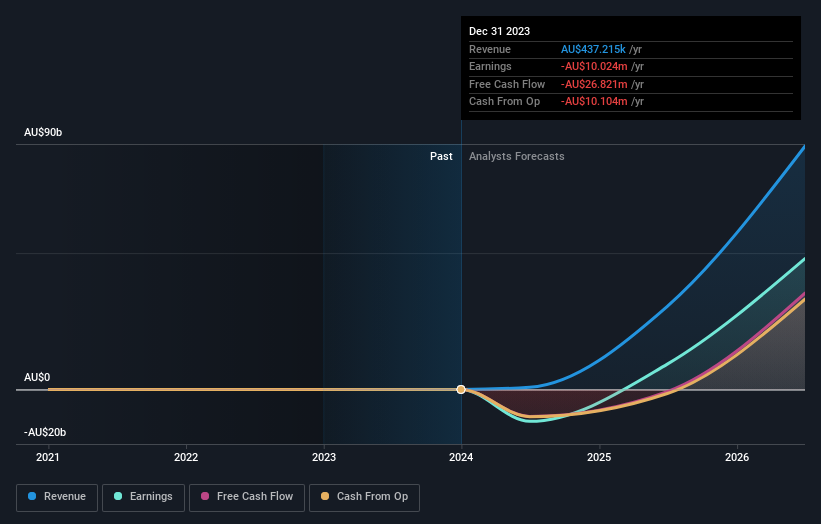

IperionX

Simply Wall St Growth Rating: ★★★★★☆

Overview: IperionX Limited is a company focused on the exploration and development of mineral properties in the United States, with a market capitalization of approximately A$669.58 million.

Operations: The firm is primarily involved in the exploration and development of mineral properties in the United States.

Insider Ownership: 14.0%

IperionX is poised for rapid expansion with revenue expected to increase by 76.4% annually, outstripping the Australian market's 5.3%. Despite generating less than US$1m currently, it's set to become profitable within three years. Recent dilution and a low forecasted return on equity of 11.7% present challenges. The firm recently raised A$50 million through an equity offering priced at A$1.91 per share and secured significant partnerships in the defense and industrial sectors, enhancing its growth prospects.

Dive into the specifics of IperionX here with our thorough growth forecast report.

Our expertly prepared valuation report IperionX implies its share price may be too high.

Where To Now?

Navigate through the entire inventory of 91 Fast Growing ASX Companies With High Insider Ownership here.

Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include ASX:BFGASX:BOT and

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com