Yahoo Finance

Yahoo Finance Analyzing Disney Stock with Q1 Earnings Looming

Disney DIS shares have climbed 27% to start 2023 with the company scheduled to release its first-quarter fiscal 2023 earnings report on Wednesday, February 8.

After such an impressive and extensive rally, the report will be critical to any further upside left in Disney stock in the near term. And investors may be pondering what lies ahead for the media and entertainment conglomerate.

Let’s take a look at what’s going on with Disney stock in the week leading up to its fiscal Q1 report.

Momentum

After a tremulous 2022 for many tech and consumer discretionary stocks, these equities have rallied to start the new year as signs of inflation beginning to ease have served as a catalyst along with the possibility of a less hawkish fed.

This has led to Disney and Netflix NFLX, its primary competitor in terms of streaming content, both skyrocketing in the last month, with their Consumer Discretionary sector up +18% year to date. Still, Disney’s performance over the last three months has lagged behind its Consumer Discretionary peers, making its fiscal Q1 report crucial to regaining its dominance in the sector.

Image Source: Zacks Investment Research

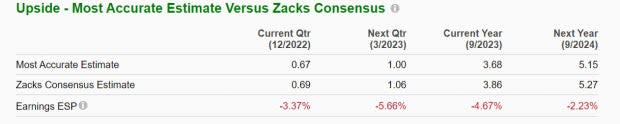

Quarterly Estimates

The Zacks Consensus for Disney’s Q1 earnings is $0.69 per share, which would be a -35% decline from Q1 2022 EPS of $1.06. Also, with the Most Accurate Consensus at $0.67 per share, this indicates that Disney could fall short on its bottom-line expectations by -3.37%.

On the top line, Q1 sales are forecasted to be $23.33 billion, up 7% from the prior year quarter. This reflects that Disney continues to struggle with tougher operating conditions and broader economic challenges as its bottom line is expected to dip despite YoY quarterly sales growth.

Image Source: Zacks Investment Research

Overall, Disney earnings are expected to rise 9% in FY23 and climb another 36% in FY24 at $5.27 per share. However, earnings estimate revisions have continued to decline over the last quarter. Sales are forecasted to be up 9% in FY23 and rise another 7% in FY24 to $97.11 billion.

Image Source: Zacks Investment Research

Subscriber Growth

Along with overall top and bottom-line growth, Wall Street will be monitoring the growth of Disney’s streaming services among its Direct-to-Consumer segment. While its Direct to Consumer services are not profitable yet, subscriber growth has been very intriguing in terms of the long-term outlook it could have for the company.

However, last quarter the operating loss among the segment increased from - $0.8 billion to -$1.5 billion, and it will be important to see if Disney was able to contract these losses during Q1.

The increase in the operating loss was due to a higher loss among Disney+ and a decrease in results at Hulu. Still, the subscriber growth among Disney+ in particular continues to be compelling following its launch in 2019 with the service striving to rival Netflix subscriptions.

During Q4, Disney+ subscribers grew by 8% to 164.2 million with the company stating the service should be profitable when it reaches 260 million subscribers. Disney estimates it could hit this target by 2024 and eventually dethrone Netflix as the king of subscription videos on demand (SVODs).

Image Source: Zacks Investment Research

Valuation & Historical Performance

Trading at $110 per share and 28.5X forward earnings, Disney stock trades nicely below its decade-long high of 134.4X and closer to the median of 19.8X with its industry average at 25.2X.

Over the last year, Disney stock is still down -21% to underperform the Consumer Discretionary sectors -16%, while also lagging the S&P 500’ and Netflix’s -8% performances. In the last decade, Disney’s +105% has also trailed the benchmark, and Netflix’s stellar +1363% performance but topped the Consumer Discretionary sectors’ +51%.

Image Source: Zacks Investment Research

Bottom Line

Heading into its fiscal Q1 report, Disney stock lands a Zacks Rank #4 (Sell) at the moment. This is in correlation with the declining earnings estimates for the current quarter, Fiscal 2023, and FY24. After such an impressive start to the new year Disney stock may be due for a pullback and there could be better opportunities despite the stock still trading attractively relative to its past.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Walt Disney Company (DIS) : Free Stock Analysis Report

Netflix, Inc. (NFLX) : Free Stock Analysis Report