Yahoo Finance

Yahoo Finance 9 Things You Need To Know About Refinancing Mortgage Loans

What is home loan refinancing?

If you’re a homeowner, you may have heard of home loan refinancing – but do you know what exactly it is? Home loan refinancing refers to the process of swapping out loans, and moving your debt to a different loan with a lower interest rate.

Homeowners generally consider refinancing when they wish to take advantage of:

lower interest rates

a shorter loan tenure

the option to use home equity (the difference between the market value of the property and the outstanding mortgage balance) to cover large expenditures

Here’s how refinancing works:

Let’s say you took out a mortgage of S$500,000 at 2% to finance a property worth S$650,000. After a certain period of time, your outstanding loan balance becomes S$300,000 and your home value appreciates to S$750,000. You notice that another home loan package is offering a lower interest rate of 1.5%.

Due to these developments, you want to refinance your home loan. You could apply for up to 75% of the current market value of your home, depending on the bank policy. That sums up to roughly S$562,500, which is more than your outstanding loan balance.

If you apply for the maximum amount, or any amount larger than your outstanding home loan balance, the excess money could be used for expenditures such as home renovations, debt consolidation or other things that require a big cash outflow.

However, be aware that if you borrow more than your current outstanding balance, you will increase the principal amount owed to the bank. This means more interest incurred over the tenure of your loan.

If you opt to apply for the exact amount to cover your current outstanding loan balance (in our case S$300,000), you will simply repay the old loan with the new one, with no additional cash borrowed.

This can result in lower monthly payments or shortened loan tenure with the same monthly payments. At a glance, it does makes sense to consider refinancing your home loan every time the interest rates drop.

From the comparison above, you can see how the difference of 0.5% affects the monthly repayment. It also makes a huge difference in the total interest incurred over the loan tenure. You could save about S$21,526.21 with the lower interest rate.

But what are the other things that need to be taken into account before you decide to refinance your home loan?

Costs to be aware of when considering home loan refinancing

It is important to be aware that the interest rates you pay are not the only costs associated with a loan.

The legal fees alone can cost from S$2,000 to S$3,000. On top of that, if you decide to refinance before your lock-in period is up, you need to pay a penalty fee of up to 1.5% of your outstanding loan.

Referring to the example above, the difference in monthly repayment is S$71.75 every month if you refinance your home loan. If you have paid legal fees of S$3,000 excluding the penalty fee, it will take about 42 months (S$3,000 / S$71.75) before you enjoy real savings on your outstanding loan.

The benefits of refinancing

Refinancing can be time-consuming and expensive. However, there are several potential benefits to refinancing.

1) You can save money on lower interest rates

One of the most popular reasons to refinance is to cut down on interest costs by refinancing into a new loan with a lower interest rate.

Over the long term, lowering the interest rate can result in significant savings. Saving 0.1% to 0.5% on interest rate can be incentive enough for refinancing.

2) Boost one’s cashflow

Not only can you save a huge amount of money, refinancing can lead to lower monthly repayments as compared to your existing monthly mortgage payment.

This will improve cash flow management, leaving you with more discretionary income for other expenses.

3) Change your loan type

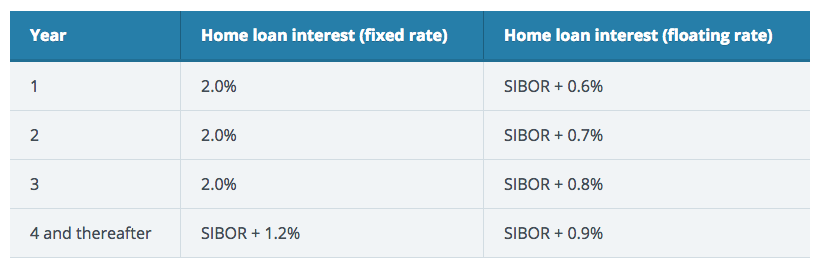

Some homeowners choose to refinance to convert their fixed rate mortgages to floating rate mortgages. Floating rate mortgages generally offer lower interest rates in a flat or declining interest rate environment.

On the other hand, fixed-rate loans generally offer a fixed rate for the first two or three years, after which it gets pegged to SIBOR or other benchmarks. They tend to be priced higher than floating-rate loans, but in a rising interest rate environment, a fixed-rate loan can save you more money in the first few years of the loan.

Here’s what a fixed-rate home plan might look like, compared to a floating-rate plan:

Who should consider mortgage refinancing?

1) People on the 4th year of their loan package, who are not under a lock-in

On the fourth year of the loan package, you may no longer be bound by your home loan’s lock-in period, which is typically 1 to 3 years. If you try to refinance during the clause, you will need to pay a penalty of typically 1.5% of the loan quantum.

For instance, if you have a loan of S$1,000,000, you will need to pay S$15,000 in penalty. If refinancing is still your best option, speak to a mortgage broker to understand the pros and cons specific to your situation.

2) Investors that plan to sell in the short term

If you’re planning to sell the property in the next five to seven years, you don’t need to be overly concerned with the 4th year rates. What you can do is to look for a home loan package that comes with the lowest rates for the first three years and actively look into a cheaper package on the fourth year.

With refinancing, you’re planning to take advantage of lower interest rates to lower your monthly repayment. By switching to a package that offers a lower interest rate, you can potentially cover your instalment with your monthly rental, or even pocket the difference.

3) Homeowners who need cash

If you refinance your home loan after your property value has increased considerably, then you can choose to cash out your home equity. However, it’s only for private properties such as condominiums and landed houses – not for HDB flats.

What it means is that you’re refinancing your mortgage for more than you’re currently owe. You can take out the difference in cash.

For instance, you bought your house a few years ago and have been paying the loan. Over the years, the property’s value has increased.

Now you owe S$300,000 on a house that’s worth S$1.6 million. You have recently looked up mortgage rates and have discovered that you can find a lower rate if you refinance.

In this situation, you can refinance for more than the S$300,000 you currently owe. If you need S$500,000 cash, you could refinance for $800,000.

You would now owe S$800,000 on your mortgage where you cash out S$500,000 in cash, and the balance S$300,000 is used to repay your old loan.

However, the refinancing process would be the same as applying for a home loan where you need to prove your ability to service the loan by providing the usual documentation of income, assets and debts.

Tips on refinancing your home loan

1) Monitor the lock-in period

If you refinance your home loan after the lock-in period expires, you would still have to bear higher repayments for a minimum of the next three months due to the notice period requirement. If you monitor your lock-in period, you would be able to apply for refinancing earlier.

The best time to refinance is to do it four to seven months ahead of the lock-in expiry.

2) Switch banks for a better offer

We would suggest calling your bank to negotiate for the best refinancing offer, but of course, you need to do your homework by looking elsewhere for a better deal and counter the offer.

3) Improve your TDSR

The Total Debt Servicing Ratio (TDSR) is a framework to ensure that people borrow and banks lend responsibly. The TDSR limits the amount borrowers can spend on debt repayments to 60% of their gross monthly income. It was introduced to ensure loans are only issued to individuals who can actually afford them.

Improve your TDSR by clearing up some of your other debts. It’s advisable to do so a month or two ahead so that it shows on your credit report.

To wrap things up, home loan refinancing needs to be considered carefully before making a decision.

Refinancing can have a positive impact on your pocket if it lowers the payments for your mortgage, decreases the tenure of your loan or boosts your home equity.

Before you decide to refinance, it is important that you understand your current financial situation and ask yourself whether it’s worth it the effort.

This article was first published on iMoney.sg, a financial comparison website for personal finance products.

See Also:

Singapore Property for Sale & Rent, Latest Property News, Advanced Analytics Tools

Here’s What You Should Know Before You Pay Off Your Home Loan Early

Real Estate Investment Trust vs Physical Properties, Which Suits You?

How To Prepare For Rising Home Loan Interest Rates In Singapore

En Bloc Calculator, Find Out If Your Condo Will Be The Next en-bloc