Yahoo Finance

Yahoo Finance 5 Charts That Explain Why Canopy Growth Is My Favorite Marijuana Stock

Canopy Growth (NASDAQOTH: TWMJF) is Canada's biggest marijuana company, and its sales could skyrocket once Canada's recreational marijuana market opens for business. Are this company's best days ahead of it? Here are five charts that show why I think the answer to that question is yes.

Chart No. 1: Cannabis consumers on the rise

According to Health Canada, the number of medical marijuana licenses in Canada has climbed to over 230,000, and as a result, Canopy Growth is serving more people than ever.

IMAGE SOURCE: CANOPY GROWTH.

In its most recent quarter, Canopy Growth sold medical marijuana products, including oils and soft-gel capsules, to 69,000 people, more than double the number it sold to in the same quarter one year ago. Over time, Health Canada -- the nation's marijuana regulator -- thinks 450,000 patients could be using medical cannabis. If that forecast is correct, then a lack of demand shouldn't be a problem for this company.

Author's chart.

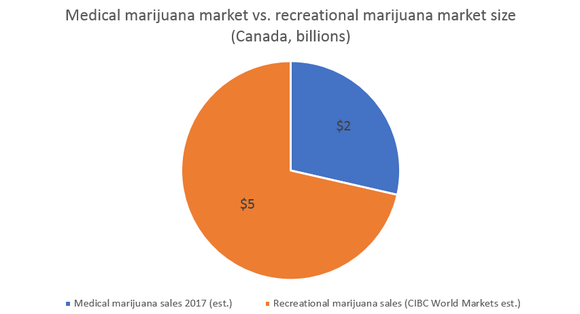

Chart No. 2: Big money at stake

Canopy Growth has an opportunity to sell more medical marijuana to more patients, but it also has a much bigger opportunity to sell marijuana to recreational users.

The company's 30% plus medical marijuana market share could indicate it has the brand recognition necessary to win recreational market share when Canada's recreational market opens for business this summer. Estimates for how big of an opportunity Canada's recreational market could be vary, but CIBC World Markets thinks it could exceed $5 billion. If it's anywhere near that big, it would dwarf Canada's medical marijuana market, which GreenWave Advisors' Matt Karnes estimates was approximately $2 billion last year.

Data source: CIBC World Markets & GreenWave Advisors. Author's chart.

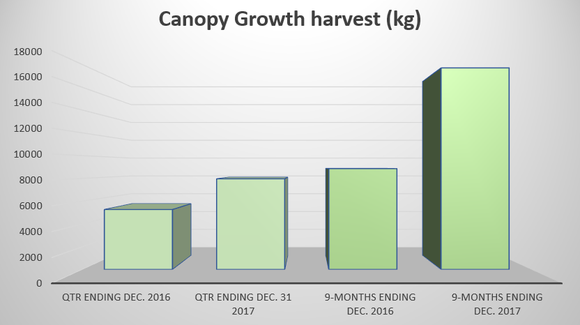

Chart No. 3: Production preparation

Serving a much larger recreational market will require significantly more production capacity. Fortunately, Canopy Growth has made big investments to expand marijuana production, and that's translating into significantly larger marijuana harvests. Last quarter, its marijuana harvest was up 51.2% year over year.

With 600,000 square feet of licensed indoor and greenhouse production capacity already, and plans for up to 5 million additional square feet in the works, I think Canopy Growth should be able to meet the expected increase in demand from recreational marijuana users.

Author's chart.

Chart No. 4: Rising revenue

The Canadian marijuana market is growing quickly, but Canopy Growth faces stiff competition that could chip away at its revenue.

For example, Aurora Cannabis (NASDAQOTH: ACBFF) and Aphria Inc. (NASDAQOTH: APHQF) are two of its biggest competitors, and each is making investments to increase their grow capacity. Aurora expects to complete an 800,000-square-foot expansion by the middle of this year, and Aphria expects to have 1 million square feet up and running early this year. However, those competitors' efforts have yet to crimp Canopy Growth's revenue. In its recently reported fiscal third quarter of 2018, sales climbed 123% to 21.7 million Canadian dollars.

WEED Revenue (TTM) data by YCharts.

Chart No. 5: Producing a profit

Canopy Growth's focus has been on investing for future growth, not delivering shareholder-friendly earnings per share. That may change later this year, though. During an interview with the Motley Fool last year, Canopy Growth's CEO suggested the company should be able to focus more on profitability once recreational cannabis orders begin rolling in.

One reason Canopy Growth's earnings could become meaningful at that point is its operating leverage. As sales and harvests have increased, its cost of production has fallen. Not including shipping and fulfillment expenses, average weighted production costs were only $1.03 per gram last quarter, down from $1.41 per gram a year ago. This allowed the company to report net earnings of $11,014 million Canadian, $0.01 per share, last quarter, in spite of its spending to expand its licensed square feet of production space.

Author's chart.

Overall, Canopy Growth is enjoying rapid demand growth, and so far, it's been able to meet that demand and generate significant sales. Its investments to increase marijuana production and lower production costs suggest it could be very well positioned to profit from recreational marijuana sales later this year, and that's why Canopy Growth is my favorite marijuana stock to buy.

More From The Motley Fool

Todd Campbell has no position in any of the stocks mentioned. His clients may have positions in the companies mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.