4 Medical Product Stocks to Buy From a Prospective Industry

The Zacks Medical – Products industry’s revenues are expected to continue its growth trajectory on the back of the robust demand for surgeries and procedures, launch of new products and expansion into new markets. An earlier-than-expected demand for respiratory products is also boosting sales. The industry players are raising the prices of their products and services to cope with the higher costs, thereby benefiting the top and bottom lines.

Meanwhile, a potential rise in budgets of U.S. hospitals amid improving demand and lower interest rates are likely to boost medical product sales going forward. However, the industry continues to face challenges due to supply-chain constraints, increased material costs and a shortage of workers in certain markets. Although the industry players have seen a sales recovery in the past few quarters, the ongoing headwinds hurt margins. The lower demand for COVID-19-related products is having a negative impact on revenues. A soft Chinese market is impeding revenue growth.

Industry participants like Boston Scientific BSX, Baxter International BAX, Haemonetics HAE and Phibro Animal Health PAHC have adapted to changing consumer preferences, and the majority of them are witnessing a rise in share price. These companies also carry a favorable Zacks Rank.

Industry Description

The industry includes companies providing medical products and cutting-edge technologies for healthcare services. These companies are primarily focused on research and development and cater to vital therapeutic areas like cardiovascular, nephrology and urology devices.

The rise in the procedure volume is benefiting sales, especially that of surgery products and services. Meanwhile, cost-cutting initiatives are helping the companies improve their bottom-line performance.

However, supply-chain disruptions amid ongoing wars continue to persist, affecting the availability of certain materials used to develop medical-related products like semiconductor chips. The inflationary pressure and labor shortages weigh on the industry players’ gross and operating margins. The trend is likely to persist in 2024, albeit weaker.

Major Trends Shaping the Future of the Medical Products Industry

AI, Medical Mechatronics & Robotics: The rising adoption of minimally-invasive robot-assisted surgeries, self-automated home-based care, use of IT in facilitating quick and improved patient care, and the shift of the payment system to a value-based model underscore the growing influence of AI in the Medical Products space. In fact, mechatronics — a high-end technology incorporating electronics, machine learning and mechanical engineering — is rapidly becoming a defining characteristic of the space. Several companies have shown substantial prowess in AI, robotics and medical mechatronics.

Advancements in robot-assisted surgical platforms continue to be crucial with respect to minimally invasive surgeries that help reduce the trauma associated with open surgery. With respect to Mechatronics, the benefits of the same have been demonstrated in the form of 3D printing, which has altered the face of the medical devices industry. Currently, 3D printing is being used to print stem cells, blood vessels, heart tissues, prosthetic organs and skin.

Rising Demand for IVD: The COVID-19 pandemic led to a rise in global demand for diagnostic testing kits in order to curb the spread of the virus. Testing became the need of the hour and led to a shift in the pipeline of IVD products, with a large number of rapid, point-of-care devices going into development. Diagnostic kit-makers not only received emergency use authorization from the FDA but also bolstered production to aid testing shortages. The industry players anticipate significant demand for rapid diagnostic testing in the future and are poised to capitalize on the same.

Emerging Markets Hold Promise: Given the rising medical awareness and economic prosperity, emerging economies have been witnessing solid demand for medical products. An aging population, relaxed regulations, cheap skilled labor, increasing wealth and the government’s focus on healthcare infrastructure make these markets extremely lucrative for global medical device players.

Zacks Industry Rank

The Zacks Medical Products industry falls within the broader Zacks Medical sector.

It currently carries a Zacks Industry Rank #63, which places it in the top 25% of more than 250 Zacks industries.

The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all member stocks, indicates bright near-term prospects. Our research shows that the top 50% of the Zacks-ranked industries outperform the bottom 50% by a factor of more than 2 to 1.

Before we present a few medical product stocks that you may want to consider for your portfolio, let’s take a look at the industry’s recent stock-market performance and valuation picture.

Industry Performance

While the industry has outperformed its own sector, it underperformed the Zacks S&P 500 composite in the past year.

Stocks in this industry have collectively risen 21.6% compared with the Zacks Medical sector’s growth of 12.3%. The S&P 500 has increased 31.2% in the same time frame.

One-Year Price Performance

Industry's Current Valuation

On the basis of the forward 12-month price-to-earnings (P/E), which is commonly used for valuing medical stocks, the industry is currently trading at 22.2X compared with the S&P 500’s 21.8X and the sector’s 23.3X.

Over the last five years, the industry has traded as high as 29.8X and as low as 18.1X, with the median being at 22.8X, as the charts show.

Price-to-Earnings Forward Twelve Months (F12M)

Price-to-Earnings Forward Twelve Months (F12M)

4 Promising Medical Product Stocks

Boston Scientific manufactures medical devices and products used in various interventional medical specialties worldwide. The company has adopted organic as well as inorganic routes for success. It generates revenues from the sale of Medical Devices reported under two segments — MedSurg and Cardiovascular. Boston Scientific is one of the leading players in the interventional cardiology market with its coronary stent product offerings.

BSX successfully continues with its expansion of operations across different geographies outside the United States. Within its international regions, the company is putting additional efforts to expand its foothold in emerging markets that hold strong growth potential. In the second quarter of 2024, despite geopolitical weaknesses, emerging markets registered sturdy growth, primarily on the back of continued broad-based momentum across BSX’s business and investment in this region.

Strong worldwide demand for its Electrophysiology and Structural Heart lines, traction in Europe for its next-generation WATCHMAN FLX, as well as contributions from accretive acquisitions are important growth drivers. The Pain and Brain franchisees are expected to gain solid traction in 2024 on the back of the strong execution of core growth strategies. The Electrophysiology arm received a strong boost on the FDA approval for FARAPULSE.

However, mounting costs due to worldwide geopolitical issues are major concerns. FX headwinds continue to largely offset the company’s performance. Full-year net sales growth is expected to be 13.5-14.5% on a reported basis and 13-14% on an organic basis. Full-year adjusted EPS is anticipated to be in the range of $2.38-$2.42.

For this Natick, MA-based company, the Zacks Consensus Estimate for 2024 revenues indicates a year-over-year improvement of 14.2%. The consensus estimate for earnings indicates growth of 17.1%. It delivered a trailing four-quarter earnings surprise of 7.18%, on average. Presently, the company carries a Zacks Rank #2 (Buy).

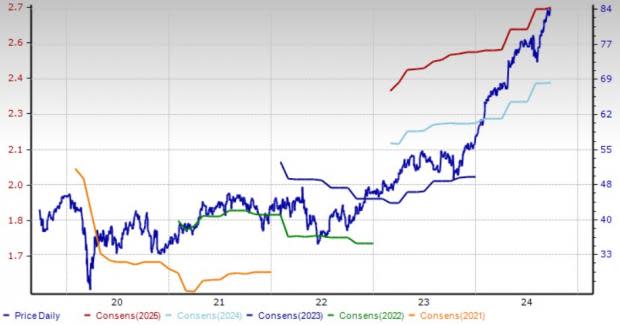

Price and Consensus: BSX

Baxter, a global medical technology company, is engaged in the development, manufacture and sale of a broad range of products, digital health solutions and therapies used by hospitals and other care-giving organizations, including at-home physician supervision. Currently, the company has presence in more than 100 countries.

Strong demand for Injectables & Anesthesia and Drug Compounding is likely to drive the top line going forward. Robust growth rates across all geographies buoy optimism. The company expects the demand for its medically essential products to continue amid a stabilizing macroeconomic climate and healthcare marketplace. Transformational actions will likely boost its performance going forward.

Increasing hospital admissions and rising procedural volume, coupled with higher alternate sites of care, are likely to drive the company’s prospects for the rest of 2024 and beyond. Moreover, capital spending by hospitals is improving in 2024, which will likely drive demand for related products. For full-year 2024, sales growth is expected to be 3% on a reported basis as well as at cc. Adjusted EPS is projected to be in the band of $2.93-$3.01.

However, the challenging macroeconomic scenario and the lingering impact of COVID-19 in some markets where Baxter competes, specifically the Asia Pacific, are driving higher-than-anticipated inflation in terms of raw materials. The company is also facing higher freight and labor charges, hurting its gross margin.

For this Deerfield, IL-based company, the Zacks Consensus Estimate for 2024 revenues indicates a year-over-year improvement of 1.8%. The consensus estimate for earnings indicates growth of 13.9%. It delivered a trailing four-quarter earnings surprise of 3.74%, on average. Presently, the company carries a Zacks Rank of 2. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

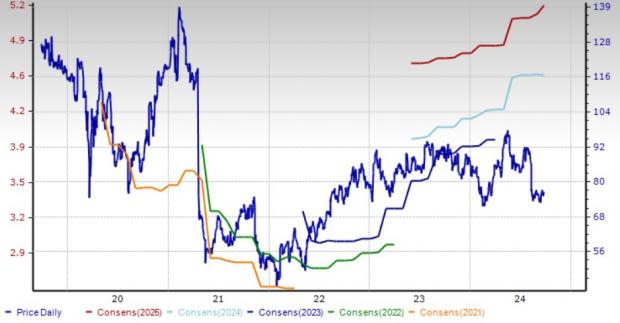

Price and Consensus: BAX

Haemonetics provides blood management solutions to its customers, including blood and plasma collectors, hospitals and health care providers globally. The company’s portfolio of integrated devices, information management and consulting services offers blood management solutions for each facet of the blood supply chain.

The company’s consistent growth performance over the past few quarters reflects its strategic focus on establishing leading positions in high-growth markets to generate solid financial returns. Strong momentum in U.S. collections and prices drove the robust volume growth and price benefits in the Plasma business. The rollout of Persona technology continued to gain momentum, with more than 25 million collections. The continued momentum in the Hospital business with new account openings and improving utilization throughout the United States is encouraging.

However, uncertainty around inflationary pressures, rising interest rates and macroeconomic conditions have increased the risk of creating new or exacerbating existing economic challenges for Haemoentics. While HAE adopted strategies like cost containment measures, selective price increases and other actions to offset these inflationary pressures in its global supply chain, it may not be able to offset all the increases in its operational costs completely.

For fiscal 2025, it expects total GAAP revenue growth to be in the range of 5-8% on a reported basis. Organic revenue growth is anticipated to be in the band of 0-3%. HAE expects full-year 2025 adjusted EPS to be in the range of $4.45-$4.75. Currently, HAE carries a Zacks Rank #2.

For this Kalamazoo, MI-based company, the Zacks Consensus Estimate for fiscal 2025 revenues is pegged at $1.39 billion. The consensus mark for earnings is pinned at $4.57 per share. The company delivered a trailing four-quarter average earnings surprise of 3.46%.

Price and Consensus: HAE

Phibro Animal Health is a leading global diversified animal health and mineral nutrition company. It provides a broad range of food animal products, including poultry, swine, beef, and dairy cattle and aquaculture.

Phibro’s Animal Health business benefits from the introduction of high-value new products in the vaccine product line. The company has been strategically investing in vaccines, nutritional specialties and companion animals to capitalize on growth opportunities. With its extensive global presence, Phibro has a strong potential to expand into emerging markets. We expect the company’s revenues to witness a 19% CAGR during fiscal 2025-2027.

However, Phibro’s Performance Products division grapples with the industry’s tough macroeconomic conditions. The ongoing regulatory issues with one of its prime products, Mecadox, raise our concern. Moreover, the increasing use of generic products by Phibro’s customers could hamper the company’s performance. The company expects net sales to be between $1.04 billion and $1.09 billion. Adjusted EPS is expected to be in the range of $1.22-$1.37.

For this Teaneck, NJ-based company, the Zacks Consensus Estimate for fiscal 2025 revenues is pegged at $1.19 billion. The consensus mark for earnings is pinned at $1.44 per share. The company delivered a trailing four-quarter average earnings surprise of 4.10%.

Price and Consensus: PAHC

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Boston Scientific Corporation (BSX) : Free Stock Analysis Report

Baxter International Inc. (BAX) : Free Stock Analysis Report

Haemonetics Corporation (HAE) : Free Stock Analysis Report

Phibro Animal Health Corporation (PAHC) : Free Stock Analysis Report