Yahoo Finance

Yahoo Finance 3 Top Energy Stocks to Buy Right Now

According to estimates, $1.8 trillion was invested in energy around the world in 2017. That's down 2% from 2016 and the third straight year of global declines.

However, that trend isn't expected to continue. The global middle class is growing, and that's driving demand for energy steadily higher. It's also going to take a combination of growth in renewables and fossil fuel development to meet that need -- and that means a lot of opportunity for investors in the years ahead.

Image source: Getty Images.

To help you get started, we asked three Motley Fool contributors to make the case for their best "buy now" energy stocks, and they came back with a very diverse collection: offshore drilling specialist Ensco PLC (NYSE: ESV), wind turbine component maker TPI Composites Inc. (NASDAQ: TPIC), and renewable energy producer Nextera Energy Partners LP (NYSE: NEP).

Ensco's waiting game could deliver huge returns

Jason Hall (Ensco): Offshore oil development has seen substantial underinvestment in recent years, but it's slowly starting to turn. On Ensco's second-quarter earnings call, CEO Carl Trowell said, "The number of visible open floater tenders has increased by more than 30% since the end of 2017 and visible open jack-up tenders are up nearly 85% over the same time period."

Expectations are that total offshore spending will increase about 50% this year. But even with all of that new spending, total offshore development continues to lag historical levels, and there's still an oversupply of drilling vessels in the global fleet.

And that's kept Ensco's stock -- along with most of its offshore peers -- trading for a substantial discount to its asset value.

ESV Price to Tangible Book Value data by YCharts.

There's reason the market continues to discount Ensco's stock price. Almost one-third of its fleet is not under contract, costing overhead to maintain but not generating any revenue. Furthermore, only 16 of its active vessels are contracted beyond next March.

But Ensco's "weak" backlog is partly by design. Even with the uptick in tenders, day rates are still low, and the company isn't interested in signing long-term deals at today's rates, instead seeking short-term work during the ramp-up in spending.

If offshore spending continues increasing apace, Ensco's high-spec fleet will be high demand within a couple of years. Trading for 43% of its book value, Ensco's worth buying today and patiently holding for the recovery.

Windmills spin in cycles -- down now, but maybe soon back up again

Rich Smith (TPI Composites): Wind turbine blades-maker TPI Composites saw its stock blown away after earnings last month -- down 14% in the seven days after earnings. The stock has bounced off its bottom, but having only regained about one-third of the points it lost, there's still a lot of room to run I think, making now an excellent time to think about buying in.

After all, as fellow Fool Neha Chamaria wrote after earnings, far from falling short, TPI Composites "has the wind at its back" right now.

With $6.4 billion in total contract value awaiting fulfillment, TPI management is telling investors to expect sales growth of 20% to 25% annually over the next three years -- significantly better than management's 13% forecast for this year.

TPIC Revenue (TTM) data by YCharts.

Analysts who follow the company expect earnings to grow even more strongly -- as much as 35% per year over the next five years -- as America's demand for "green energy" only continues to grow stronger.

That means that, even with earnings temporarily depressed due to TPI starting up new production lines (to deal with the growth in demand), and TPI stock consequently selling for an apparently pricey 28.5 times trailing earnings, TPI stock could actually be a bargain for investors who buy in during this transition year.

A reliable renewable energy stock

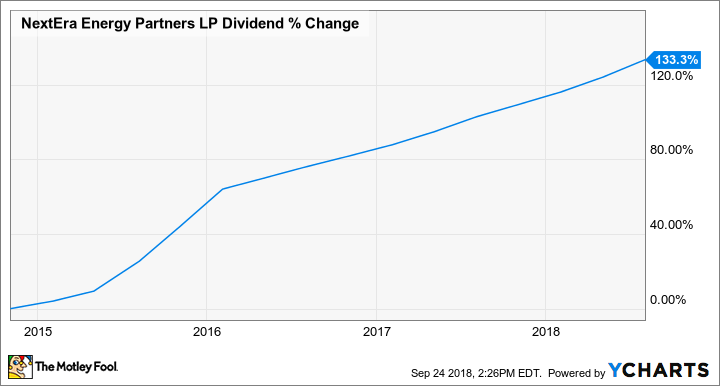

Travis Hoium (NextEra Energy Partners): A lot of energy stocks rely on commodity prices like oil, natural gas, coal, or even electricity to make money. When prices go up, they do well financially, and when they go down, it can be devastating to a business. NextEra Energy Partners isn't a commodity-dependent stock and is unique in that it owns a portfolio of renewable energy assets that have long-term contracted electricity sales to utilities. These contracts mean the company's cash flows are more like a bond than a commodity-dependent energy stock, which I think is attractive in today's market.

Right now, NextEra Energy Partners owns 4,700 megawatts (MW) of renewable energy assets with an average of 17 years remaining on sales contracts. The company's structure of paying dividends with cash flows, which is known as a return of capital from a tax perspective, also means management expects dividends will be tax-free for at least the next eight years and corporate taxes will be negligible for at least the next 15 years.

NEP Dividend data by YCharts.

In the yieldco space, where NextEra Energy Partners operates, it holds an advantage because of the backing of its parent utility, NextEra Energy, and benefits from a relatively low dividend yield of 3.6%. The low yield allows management to issue stock to buy assets that are accretive to the dividend over the long term, allowing flexibility in financing renewable energy assets. Given management's expectation that NextEra Energy Partners' dividend will grow 12% to 15% through 2023, the low dividend yield may not last for long, making this a great long-term buy.

More From The Motley Fool

Jason Hall owns shares of Ensco. Rich Smith owns shares of TPI Composites. Travis Hoium owns shares of NextEra Energy Partners. The Motley Fool recommends TPI Composites. The Motley Fool has a disclosure policy.