Yahoo Finance

Yahoo Finance 3 Picks From a Strengthening Ecommerce Industry

This year is likely to see a return to normalcy with ecommerce taking away bigger and bigger slices of the total retail pie. The trend started last year itself, as can be seen from the third-quarter (last-reported) data from the Commerce Department: ecommerce sales in the third quarter grew 10.8% over 3Q21 (up 3.0% sequentially), with total retail sales increasing 9.1% (up 0.7% sequentially). Ecommerce accounted for around 14.1% of total U.S. retail sales.

As the back-to-stores trend recedes, convenience is returning as a major factor driving volumes in this industry and this is particularly true of Gen-Z, which is becoming a more relevant contributor to sales. Many of these buyers have grown up on the Internet and take a much higher level of digitization as normalcy. They are also likely to hang out on popular social media platforms, allowing themselves to be influenced by the latest trends there. This is driving an entirely new perspective on the ecommerce space, one that is likely to expand with more advanced technology such as AR/VR and the Metaverse.

Valuation although down over the past year, remains expensive, reflecting the relatively stronger growth prospects. A large number of stocks in this extremely diverse industry are worth buying today, but we’ve picked three: Alibaba (BABA), Expedia (EXPE), MercadoLibre (MELI).

About The Industry

Internet - Commerce continues to evolve as the technologies driving it advance.

On the one side are increasingly powerful and capable user devices. On the other are sophisticated, AI-enabled software platforms facilitating transactions that are thereby, more capable of delivering user satisfaction. Social commerce and chatbots are further facilitating things.

Differentiation comes from better technology for improved showcasing, easier navigation and payment, speedier delivery and returns, brand building, comparison shopping, loyalty, etc. as well as more shipping options, which generally tip the scales in favor of larger players. Particularly because there is fierce price competition necessitating deep discounting, which keeps prices down.

Current Trends Driving the Internet-Commerce Industry

Macro conditions should continue to improve for the industry, which has been mired for the most part in 2022 by a combination of factors, including a consumer trend back to stores, as well as generally tighter purse strings as people fretted about rising costs and the possibility of a recession that would see significant job losses. But things appear to be clearing up in 2023 with inflation coming down (however slowly), a recession looking less and less likely and people going back to the convenience of online shopping. To top it all, the jobs scenario looks as strong as ever despite the tech layoffs. For producers, supply chain issues have alleviated while the labor situation is still tight. Global uncertainties continue to affect foreign exchange effects for companies with international operations. The higher interest rate is another pressure on producers, and by extension consumers, which is another negative for the year. Therefore, the digital infrastructure that retailers have been building up in the last few years will disproportionately increase profitability this year. The importance of having a digital presence has never been greater, particularly considering the fact that the retail ecommerce market continues to expand into new product segments and geographies.

Ecommerce will continue to gain at the expense of brick-and-mortar this year. The Commerce Department’s data for the last available quarter (3Q22) shows that ecommerce growth was already moving past overall retail sector growth in that quarter when the back-to-store trend was also operational. Therefore, this year is likely to be a relatively normal year, which means that ecommerce will continue to grow at the expense of physical stores. Shopify’s Michael Keenan agrees with this analysis. According to a recent statement of his, “Two years ago, only 17.8% of sales were made from online purchases. That number is expected to reach 20.8% in 2023, a 2-percentage point increase in e-commerce market share. Growth is expected to continue, reaching 23% by 2025, which translates to a 5.2 percentage point increase in just five years.”

Ecommerce growing at the expense of physical stores doesn’t mean that a physical presence will be downgraded. In fact, with Gen Z entering the marketplace, the demand for convenience and options will remain paramount. In many cases, this will mean faster deliveries or pickups from some nearby convenient location. Since it is only proximity to a consumer that can facilitate quick delivery, both ecommerce pureplays and traditional retailers will continue to balance ecommerce sales with a physical presence. Therefore, a hybrid/omnichannel model will remain of utmost importance, allowing customized, quick and convenient delivery (BOPIS, curbside pickup) through apps. Customers generally downgrade stores that don’t provide these conveniences. Self-driven delivery vehicles and drones are also on the horizon to deal with logistics problems and make deliveries smoother and cheaper.

A trend that Gen-Z is popularizing now is social commerce. Social commerce means the ability to discover, research, buy and checkout on a social media platform. Brands usually have store fronts on these platforms where influencers also discuss their products, thus driving traffic to them. The social element of shopping that ecommerce had taken out is thus returning through this route. Since social commerce is already popular in China, it isn’t surprising that the Chinese social media platform TikTok that’s also very popular with Gen Z is the number one place for social commerce. But others like Facebook and Instagram are also in the game. According to The Future of Commerce, “Global sales via social media platforms were estimated at 992 billion U.S. dollars in 2022, and forecasts suggest that social commerce sales will reach around 2.9 trillion U.S. dollars by 2026. Social commerce is critical for brands to reach their target audiences, and is expected to generate $30.73 billion in sales in 2023, accounting for 20% of global retail e-commerce.” Other trends online retailers are focused on include grocery sales and the buy-now-pay-later option.

Also, data mining has never been easier. Because of the many details involved in satisfying a customer, data mining has grown in importance over the years, with the party controlling the customer’s data being best positioned to identify and service demand while also delivering the desired experience. Most of the big ecommerce players are also into payments processing, which gives them further insight into a customer’s tastes, preferences and buying habits. As machines read and process this data, they can create

Zacks Industry Rank Reflects Ongoing Strength

The Zacks Internet - Commerce Industry is a rather large group within the broader Zacks Retail And WholesaleSector. It carries a Zacks Industry Rank of #34, which places it in the top 14% of 250 Zacks industries.

Our research shows that the top 50% of the Zacks-ranked industries outperforms the bottom 50% by a factor of more than 2 to 1. So the group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates relatively strong near-term prospects.

The industry’s positioning in the top 50% of the Zacks-ranked industries is the result of its relative performance versus others. What we’re seeing in the aggregate estimate revisions is significantly weaker earnings than a year ago. However, expectations for both 2022 and 2023 (2022 results are not all in yet) are off just 3 cents since October, indicating that the return-to-store trend is stabilizing. As things stand now, the aggregate earnings estimate for 2022 is down 38.4% and for 2023 is down 44.9%. Profitability is improving, despite constantly rising SG&A, possibly because some of the store traffic related to the reopening has started moving back online. Supply chain and labor issues are also easing. A recession is looking increasingly unlikely, as employment numbers show no sign of softening, even as prices continue to cool.

Before we present a few stocks that you may want to consider for your portfolio, let’s take a look at the industry’s recent stock-market performance and valuation picture.

Industry Lags On Shareholder Returns

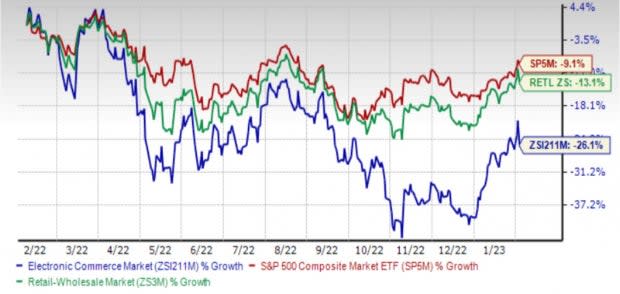

The Zacks Electronic - Commerce Industry has lagged both the broader Zacks Retail and Wholesale Sector as well as the S&P 500 index though much of the past year although it has been doing notably better than both since December.

Therefore, we see that the stocks in this industry have collectively lost 26.1% of their value over the past year, compared to the broader Zacks Retail and Wholesale Sector, which lost 13.1% and the S&P 500, which lost just 9.1%.

One-Year Price Performance

Image Source: Zacks Investment Research

Industry's Current Valuation

On the price-to-forward 12 months’ earnings (P/E) basis, the industry still looks grossly overvalued (34.34X) with respect to both the S&P 500 (18.73X) and the broader retail sector (22.73X).

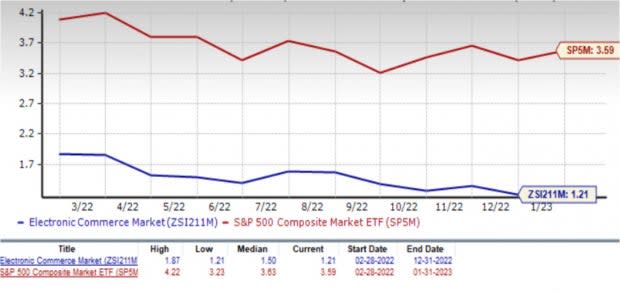

On the basis of forward sales (P/S) for the year however, the industry trades at its annual low of 1.21X, which trails the sector’s 1.25X (close to its median level) as well as the S&P 500’s 3.59X (also relatively close to its median value). Over the past year, the industry has traded as high as 1.87X, as low as 1.21X and at the median of 1.50X, as the chart below shows.

Forward 12 Month Price-to-Sales (P/S) Ratio

Image Source: Zacks Investment Research

3 Stocks Worth Considering

While the industry’s valuation looks kind of prohibitive, there are quite a large number of stocks that are currently ripe for the picking. That’s because of the significant variety that exists in this industry in terms of lines of business, business model, location, and so forth. All of the following stocks carry a Zacks Rank #1 (Strong Buy):

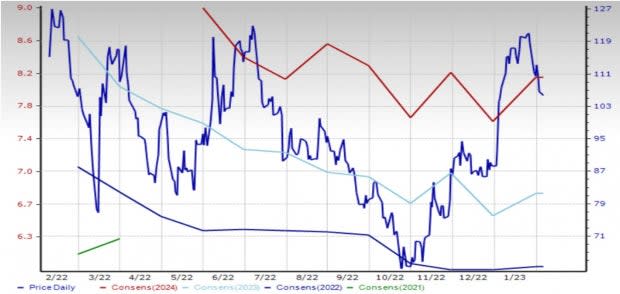

Alibaba Group Holding Limited (BABA): Like Amazon in the U.S., Hangzhou PRC-based Alibaba Group Holding Limited is a leading provider of a whole range of products and services (retail, advertising, media and entertainment, cloud infrastructure), primarily through its Chinese and international ecommerce platforms. Other than online retail platforms like Taobao Marketplace, Tmall, Alimama, 1688.com, Alibaba.com, etc. it owns and operates a retail chain called Freshippo, an import e-commerce platform called Tmall Global, an online-offline integration service for grocery and FMCG brands called Taoxianda, the Cainiao Network logistic services platform, etc. It has a platform to tap every opportunity in the ecommerce space in China, including the Taobao Ad Network and Exchange, a real-time online bidding marketing exchange and media businesses. It also provides elastic computing, storage, network, security, database and big data, and IoT services.

Chinese stocks are benefiting from the lifting of draconian measures by the government to fight COVID last year. Alibaba in particular has done better than many others because of the breadth of its offerings and innovation at every level that have helped it retain customers and add new ones. This focus, along with capacity expansion, operating efficiency and cost optimization should translate into disproportionately stronger business flow now that the market is open. Macro concerns and global uncertainties remain, but these concerns aren’t specific to Alibaba.

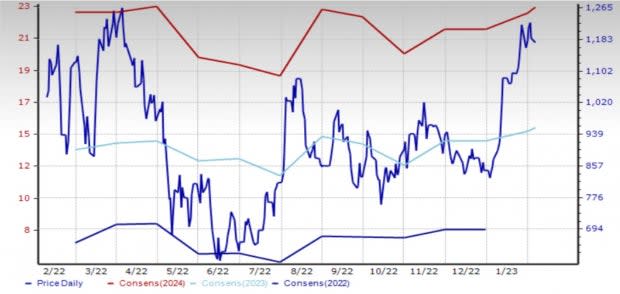

In the last 30 days, analysts have raised Alibaba’s 2023 (ending March) estimates by 7 cents and 2024 estimates by 30 cents.

The shares have lost just 7.4% over the past year, a testimony to investor confidence.

Price & Consensus: BABA

Image Source: Zacks Investment Research

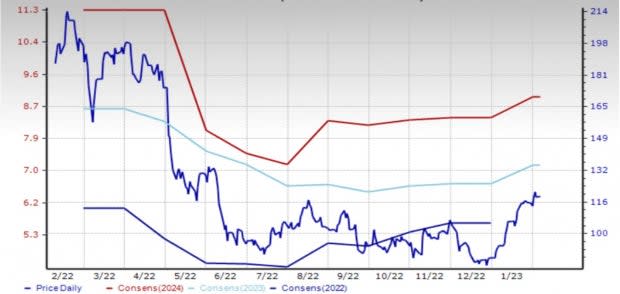

Expedia Group, Inc. (EXPE): Seattle-based Expedia is an online travel company operating through Retail, B2B and trivago segments. It serves leisure and corporate travelers. Expedia takes bookings for hotel and alternative accommodation, cruise ships, rental cars, air tickets and such other services. Through Expedia Partner Solutions, a B2B brand and Egencia, it provides corporate travel management services. It also provides advertising and media services.

As was evident through most of last year, vaccination has emboldened people, encouraging them to start traveling again. This took Expedia’s revenues to pre-pandemic levels. Growth should remain strong this year, not only because the pandemic is pretty much behind us, but also because there is some pent-up travel demand out there. The strong jobs numbers and softening inflation are also positive for travel sales this year. Expedia also has effective loyalty programs and its app-users are at all-time highs. Its focus on improving user experience through better web and app experiences will ensure that the user base continues to expand.

Analysts have raised their 2023 estimates by 40 cents in the last 30 days.

The Zacks Rank #1 stock is down 36.6% year to date, so there is much room for expansion.

Price & Consensus: EXPE

Image Source: Zacks Investment Research

MercadoLibre, Inc. MELI: Buenos Aires, Argentina based MercadoLibre is one of the largest e-commerce platforms in Latin America. Other than its online marketplaces, the company offers payments, advertising and logistics services.

The company is seeing very strong growth in its served markets, driven by overall user experience, which is a function of the selection, pricing, logistics services (speed and cost of deliveries), customer service and technology. Its steadfast investments in these areas in the face of the back-to-stores trend in the last couple of years is clearly bearing fruit. This has allowed share gains in Brazil and Chile, resilience in Mexico and strong growth in Argentina. The payments business also continues to grow strongly with continued expansion of the user base. The volumes per device is the driving factor in MPOS with devices sales being a slight drag.

In the last 30 days, analysts have raised their 2023 estimates by 60 cents. They are extremely optimistic about the company’s growth prospects.

The shares are up 13.7% in the past year.

Price Performance: MELI

Image Source: Zacks Investment Research

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Expedia Group, Inc. (EXPE) : Free Stock Analysis Report

MercadoLibre, Inc. (MELI) : Free Stock Analysis Report

Alibaba Group Holding Limited (BABA) : Free Stock Analysis Report